Fellow shareholders,

As we close out another fiscal year chock-a-block 🇦🇺 with wins, we find ourselves in a climate of widespread uncertainty. Yet despite unsettling world events and headlines reporting macroeconomic volatility, Atlassian continues to march forward with a long-term mindset, delivering top-notch products and legendary service to our customers. ![]()

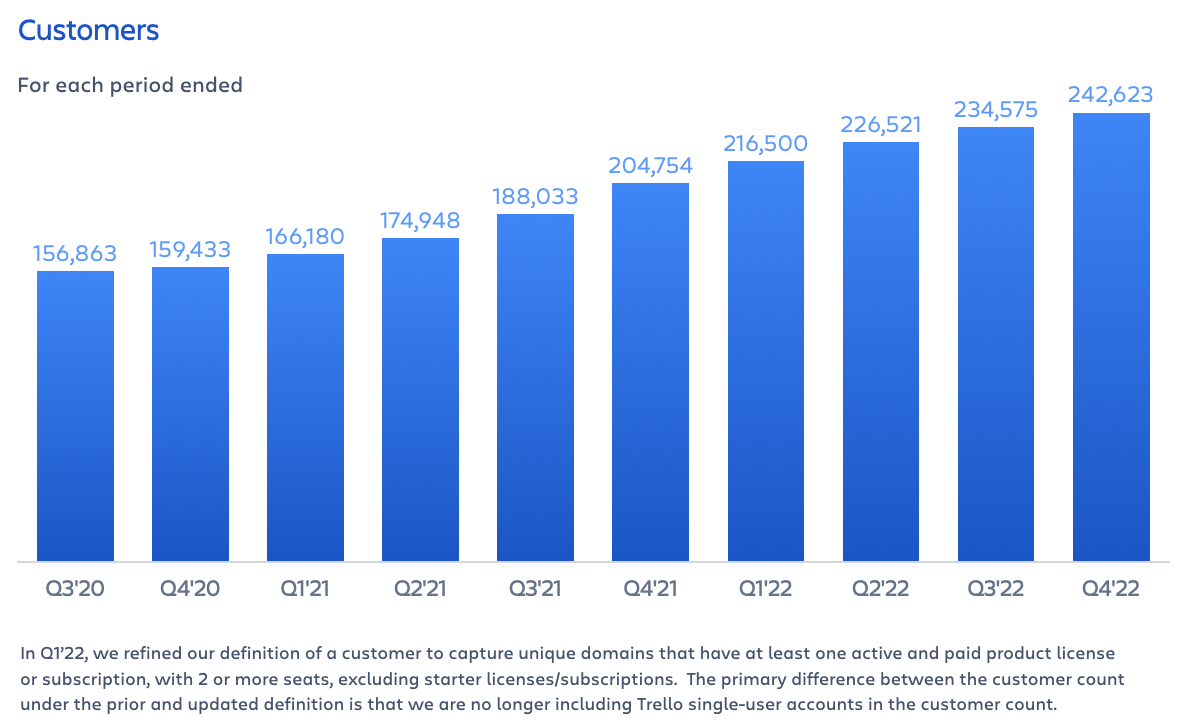

We capped off FY22 with strong Q4 results across our three markets: agile and DevOps, IT service management (ITSM), and work management. Not only did our customer base top 242,000 this quarter, but our headcount also grew by 634 with most new hires in R&D – a testament to our team’s ability to execute against ambitious hiring goals.

We firmly believe that Atlassian is uniquely positioned, having deep-seated momentum and a differentiated business model. This gives us the confidence to make incremental investments – despite the current environment – that will fuel even more durable growth over the long term and deepen our strategic advantages. We know this is an unconventional choice right now and want to be open with our investors about it.

We will remain vigilant in this environment, and while we are not insulated from broader macroeconomic pressures, there are three dynamics particular to Atlassian’s business informing our decision to press forward. First, we’ve observed over the years that developers tend to be the last roles companies scale back on. We believe this will continue to prove true, especially for the overwhelming number of organizations undergoing digital transformation. Second, whilst our products punch above their weight in terms of value, Atlassian is a relatively small line item in overall IT budgets and likely not where customers look to reduce costs. Third, customers tell us that Atlassian products are mission-critical for them. And because our products are already the low-cost option, there aren’t further savings to be had from switching to a competitor.

Again, we’ll continue to scan the horizon for warning signs and be candid with investors as we have throughout our six+ years as a public company. ![]()

As we shared at our Investor Day in April, we have a line of sight to $10 billion in annual revenue based on our current products and core markets. We believe our investments will propel us past this milestone faster, while further strengthening our strategic position. History shows that turbulent economic environments offer a chance for companies to gain market share – to shake up the leaderboard. Atlassian intends to seize this moment with all the thoughtfulness and ingenuity you’ve come to expect from us.

We can’t predict what the future holds at a macro level, but we’re forging ahead with conviction and vigilance as we keep playing offense in FY23. Our mission is to unleash the potential of every team. And right now, that’s especially important for those of our 242,000+ customers who are facing instability. We’ll continue to deliver innovative products and practices to help them find their footing quickly.

Head in the cloud, feet on the ground ⛅

Atlassian rolls into the new fiscal year with robust momentum in the cloud. We closed FY22 with over 200,000 Cloud customers, Cloud revenue growth in Q4’22 of 55% year-over-year, and a Cloud net expansion rate that topped 130% (with large customers topping 140%). Looking ahead, we expect Cloud revenue growth to continue at a healthy pace, reiterating what we’ve said previously: approximately 50% year-over-year for both FY23 and FY24, with approximately 10 points of this growth driven by migrations in both years.

Migrations to our Cloud products from on-premises instances are moving ahead at a steady clip, with Cloud migrations in FY22 up more than 2x over the prior year. This includes a growing number of enterprise customers, including the likes of Deutsche Bank and Sun Life. We’re honored to have earned their trust in our world-class, enterprise-grade platform and are keen to enhance the value they get from it over the years with new products and capabilities.

Migrating to Atlassian’s cloud-based services supports Deutsche Bank’s agile transformation. Jira Software and Confluence enable our teams to better organize their daily work, drive agile collaboration, and exchange ideas while simplifying operations and reducing costs by moving to a single platform.

– Marcus Jung, Head of End User Computing at Deutsche Bank

We frequently hear from customers who are happier than ever after migrating to Cloud. And it’s not just the admins. At Sun Life, for example, 97% of end users say they’re satisfied with our Cloud products.

We expect the enterprise migration trend to continue rolling into FY23, especially as we’ve now opened up 35,000-user Cloud instances to our entire customer base.

Extraordinary customer value is our secret sauce 🤫

At our Investor Day event in April, we shared detailed materials that explain our perspectives on our three markets, our cloud platform, and building an enduring company. We encourage all investors and stakeholders to read these materials in depth as they provide a great summary of our thinking. 📖

We’ve also shared a massive set of product updates in the past few months, both at Team ‘22 and in our Q3 shareholder letter. So this quarter, we’d like to focus on the value our customers get from Atlassian products and why we win in each of our three markets.

Agile and DevOps

This is our home turf, historically speaking. We know this audience well and have a strong reputation in this market. We understand that curating a custom toolchain is the best way to develop software, which is why developers prefer it to our competitors’ monolithic products that try to be good at everything but inevitably fall short.

We focus on being a central nervous system that connects best-of-breed tools, rather than trying to cover every use case ourselves. With Atlassian, software teams get a level of flexibility they won’t find with any other vendor. They can mix n’ match Jira Software, Bitbucket, and Confluence with dozens of 3rd-party tools that integrate seamlessly through our Open DevOps framework. We’re also delivering a steady stream of new offerings like Compass and Jira Product Discovery that connect developers with their colleagues in operations and product management.

Today, over 100,000 customers around the world use Jira Software. This highlights the massive opportunity just within our installed base of 242,000+ customers. And we’ve got the rest of the world’s software teams in our sights.

IT service management

We’ve been saying it for ages: the silos separating development and IT teams are disappearing. That’s why we’ve spent the past several years bringing dev and IT together into the same products – something Atlassian is uniquely positioned to do because we’re already known and trusted by both groups. Not to mention the fact that our Cloud products run on top of a true platform that connects users, data, and content across products.

All of which help service teams move faster. At The Telegraph UK, Atlassian products allow their IT teams to “move at the speed of the industry.” Similarly, the Yale School of Management says our products have boosted efficiency so much that they “can’t do without them” because their stakeholders have come to expect the high level of service they now provide.

Jira Service Management suits both Fortune 500 companies and startups operating out of a garage. Where our competitors’ ITSM products are far more expensive and have interminable sales cycles, we get our customers up and running in as little as a day so they can spend more time serving their customers. That’s pretty attractive in this economy. Or any economy.

Work management

As a company that embraces autonomy for its teams, Atlassian knows there are lots of ways to collaborate effectively. Our work management products offer varying degrees of structure so every team can support their preferred way of working. And thanks to products like Confluence (which had a banner year in FY22) and Atlas that go wall to wall within an organization, plus deep integrations between Trello and the Jira family of products, teams stay aligned no matter how they track their day-to-day work.

Atlassian is the only work management vendor to bridge technical and non-technical teams. Historically, we would land with a development team, then spread to their colleagues in “the business.” Indeed, 46% of Jira Software users are in non-technical roles. Today, we are increasingly landing with the rest of the organization as companies search for ways to help their teams work differently, together. We’re seeing strong growth across our work management products, with Confluence leading the way.

[Atlassian] tools help us come together and work together in a way that we can visualize and share with other team members. It’s helped us brainstorm and think outside the box, come up with exciting ideas, then turn them into processes.

– Haley Ennes, Recruitment Operations Lead at Sprout Social

Atlassian generates all this success and momentum across our three markets by doing things differently. We are prudent stewards of capital, but we’re not afraid to invest for the long term when we see a chance to further strengthen our advantages. We embrace transparency with our customers and empower them to walk through the buyer’s journey at their own pace. We scale our teams thoughtfully so we can grow sustainably. We invest more in R&D than our peers and have one of the most (if not the most) efficient GTM machines in software.

We strive to deliver more value than what customers are paying for. And they love us for it.

Team Anywhere goes wall-to-wall in India 🇮🇳

While other companies are facing record attrition, our Team Anywhere program and award-winning culture have largely shielded us from the “great resignation.” Even long-serving star performers who could have their pick of employers or perhaps even retire early are choosing to stay with Atlassian. After previously opening up New Zealand, as well as expanding within Canada and Europe, Atlassians can now work from anywhere within India. This opens up massive new talent pools to hire from and gives our existing employees in India more choice.

We’ve hired over 2,300 Atlassians globally (over a quarter of our team) over the past year, 50% of whom live more than two hours from an office location, and over 3,800 Atlassians in total over the past two years. Thanks to Team Anywhere, Atlassian has access to a much larger talent pool and can drive towards our hiring goals without lowering the bar.

Now that our offices are open again, we look forward to bringing our teams together in intentional ways that enhance collaboration, deepen our personal connections, and boost our energy. We’ll continue to provide the most flexible, inclusive work environment possible. It’s the way of the future, it’s the right thing to do, and it’s how we’ll keep attracting the best talent.

Been there, done that, came out on top 👍

Running a software company with nearly $3 billion in revenue isn’t exactly the wild-wild West, but the phrase “this ain’t our first rodeo” rings true. Atlassian started in 2002 with a $10,000-limit credit card, so we have 20 years of experience when it comes to disciplined choices and patient, long-term thinking as we look towards that $10 billion revenue milestone and beyond. And when it’s necessary, we’re not afraid to make bold, calculated moves that other companies shy away from.

We seized opportunities during the economic turbulence of 2008-2009 to scoop up talent that wouldn’t have been available otherwise and broadened our customer base by offering $10 starter licenses for our products. Today we’re echoing that approach with Free editions of our Cloud products and ambitions to more than double our headcount over the next few years. Playing offense when others were throwing off their back foot 🏈 worked for us then, and we’re confident it will work for us now.

Atlassian’s values endure no matter what the market conditions. We’ll continue to be transparent, care for our customers and teams, balance opportunity versus risk, and be the change we want to see in the world. That’s how we’ll continue to win.

Welcoming new CFO Joe Binz 👋

We are thrilled to announce that Joe Binz will join Atlassian as CFO on September 6, 2022. Joe brings more than 25 years of finance leadership and experience in the technology industry. Since 2014, he has held the role of Corporate Vice President, Finance at Microsoft, where he was responsible for leading the company’s financial planning and analysis, investor relations, acquisition integration, and procurement functions. Over his twenty-year career with Microsoft, he was a pivotal finance leader where he most notably guided the company’s business transformation through its multi-billion dollar move to the cloud. Prior to his time at Microsoft, Joe spent eight years at Intel where he held a variety of finance roles supporting manufacturing operations, product groups, and Intel Capital. He holds a Bachelor of Science in Finance from the University of Illinois Urbana-Champaign, and a Master of Business Administration from the University of Michigan’s Ross School of Business.

We’ve both enjoyed getting to know Joe over the past few months and couldn’t be more excited for him to join the TEAM.

We end FY22 with tremendous gratitude for the way our customers, partners, and employees stay focused on delivering great products and building a vibrant community around Atlassian. 💙 Here’s to the road ahead, and to unleashing the potential of every team.

– Mike and Scott

The bottom line

- Despite the current climate of uncertainty, Atlassian continues to march ahead. We have unwavering conviction in our business model, team, and ability to keep winning in our three global markets.

- Cloud migrations and revenue growth remain robust, with net expansion rate in the Cloud exceeding 130% (with large customers topping 140%).

- Our TEAM Anywhere program around remote work continues to offer our employees more flexibility and create ever-larger talent pools to hire from as we scale toward $10 billion in revenue and beyond.

Customer highlights

Atlassian continued to see healthy growth in all segments of our customer base thanks to our full ladder of Cloud product editions from Free to Enterprise. Our hyper-efficient self-serve sales funnel landed 37,869 new customers in FY22, with 8,048 coming in this past quarter. That brings our total customer count to 242,623.

Behind the scenes, our innovation machine (aka, our R&D teams) is always finding new ways to inspire and delight our customers. The incredible value we deliver keeps customers coming back for more, allowing us to expand our footprint within their walls, which creates a virtuous cycle that fuels even more R&D investment.

We continue to enhance our existing products – Jira Service Management’s new knowledge base, for example – while launching new products like Atlas and Compass that come out of our internal incubator program, Point A. Customers fired up tens of thousands of instances of our Point A products in FY22, and we’re gearing up for even more in FY23. 🔥 And we do all of this on the back of our industry-leading GTM model.

Once customers land with us, we can identify those with the highest expansion potential with surgical precision and focus our high-touch tactics on those organizations. We already serve over two-thirds of the Fortune 500, yet no one customer represents more than 1% of our total revenue. This strategy, bolstered by our ecosystem of apps that make the core products stickier, is what drives the enviable lifetime customer spend Atlassian enjoys.

See you in Septemmmber… 🎶

As Mike and Scott said above, we’ve never felt more confident about our strategies in each of our three markets, and the secular trends that reinforce them. I encourage you to watch our three market-specific keynote sessions from Team ‘22 if you missed them back in April. You’ll get to see all the latest product updates in action, and hear more about our vision for the future of agile and DevOps, ITSM, and work management.

Building on the success of Team ‘22, Atlassian is holding events tailored to each of our markets for the first time ever. We’ll kick things off in September with a work management event, Atlassian Presents: Work Life. Events for the other markets will follow later in FY23. Each event will highlight our leadership in these markets, build deeper relationships with our global audience, and give attendees an up-close view of how Atlassian products can help them collaborate more effectively.

So mark your calendars for September 29th. Whether you join us in person at the Chase Center in San Francisco, or enjoy the live streams from wherever you are, I hope you can be there as we explore how teams can work differently, together.

– Cameron

Financial highlights

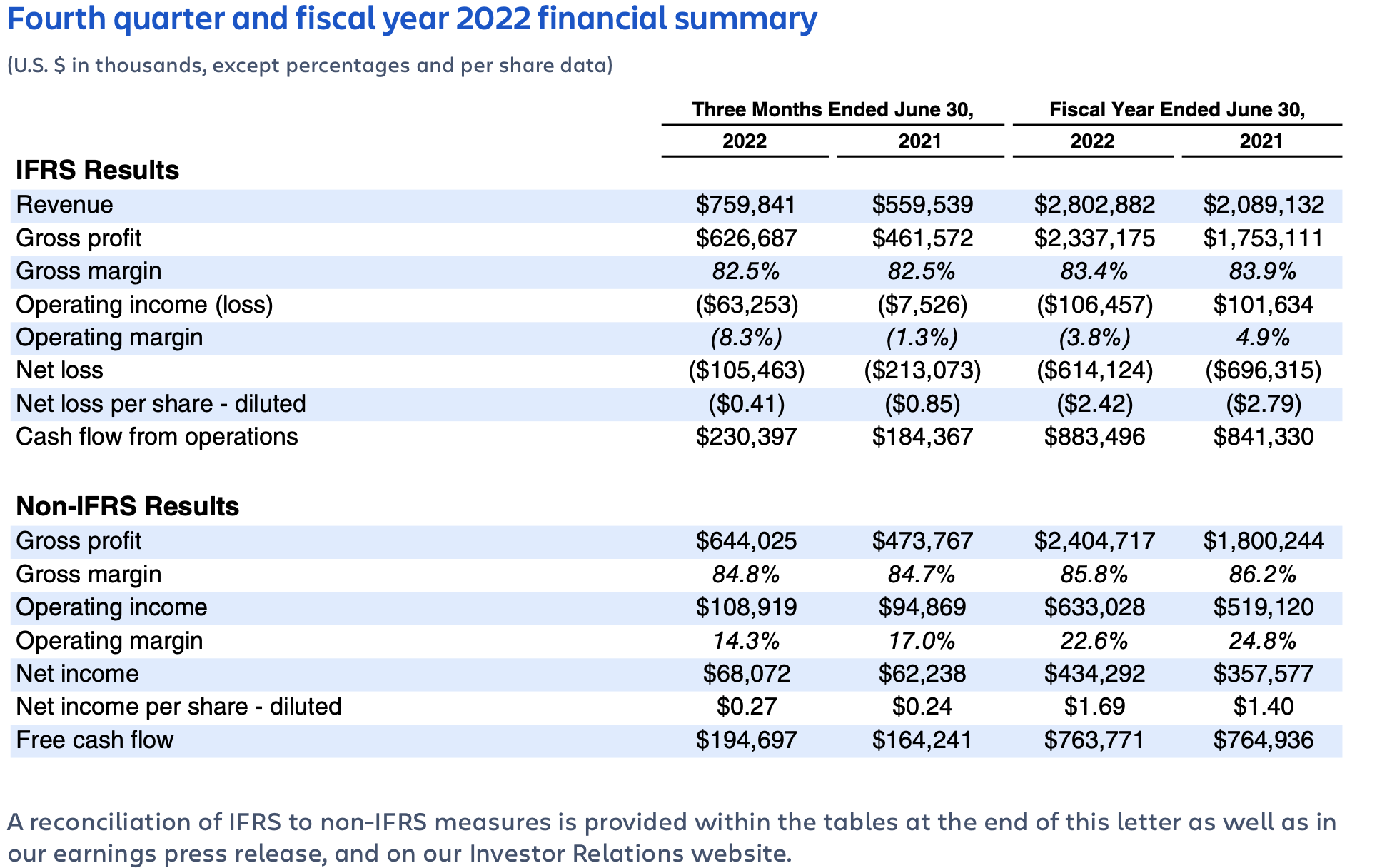

Atlassian turned in another quarter of strong financial performance in Q4’22, capping off another year of steady execution against our long-term goals. We continue to see momentum in Cloud migrations and growing demand for our products. We are entering FY23 with a clear roadmap and conviction in the sizable opportunities that we have identified.

Highlights for Q4’22 include:

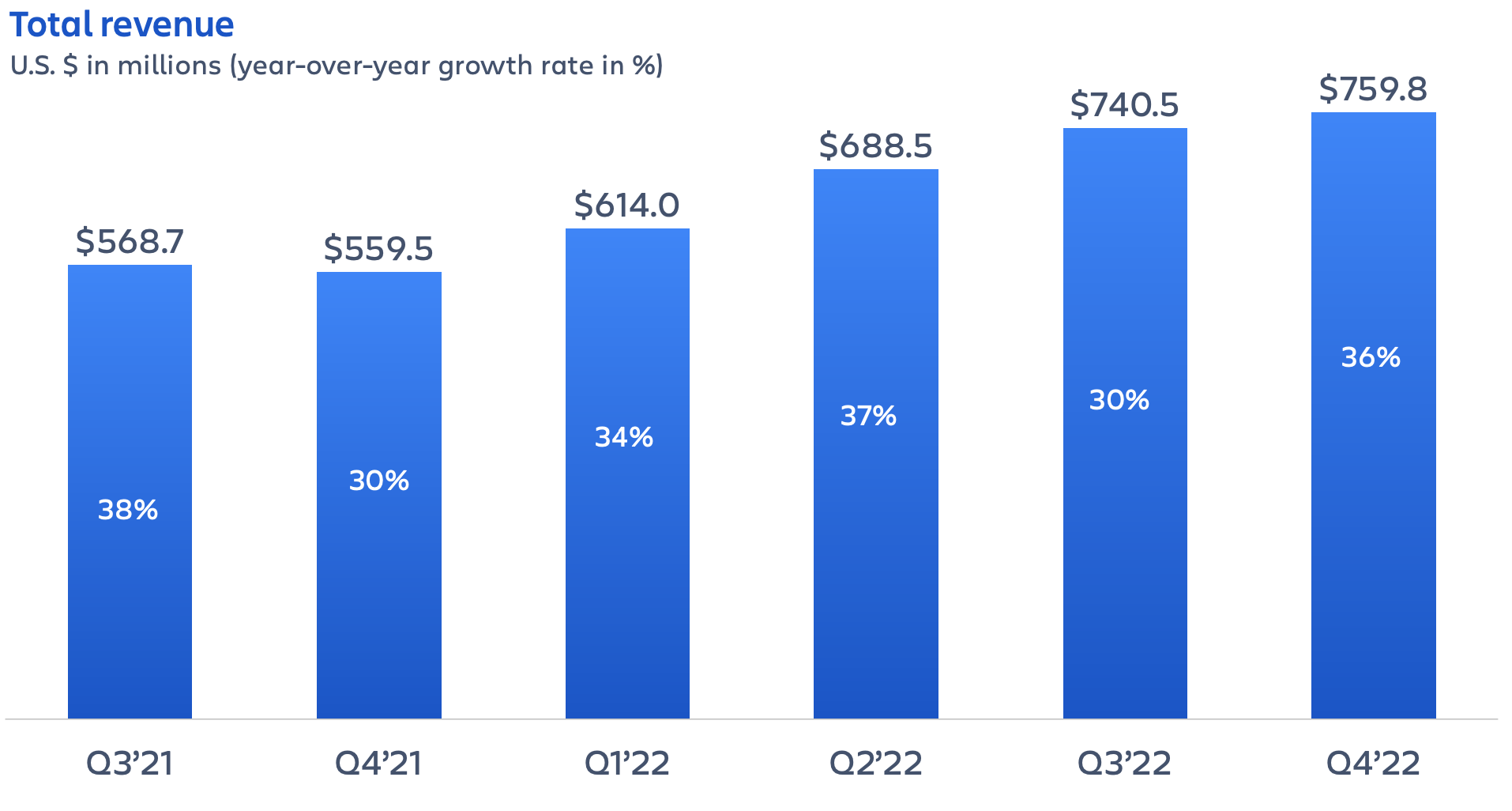

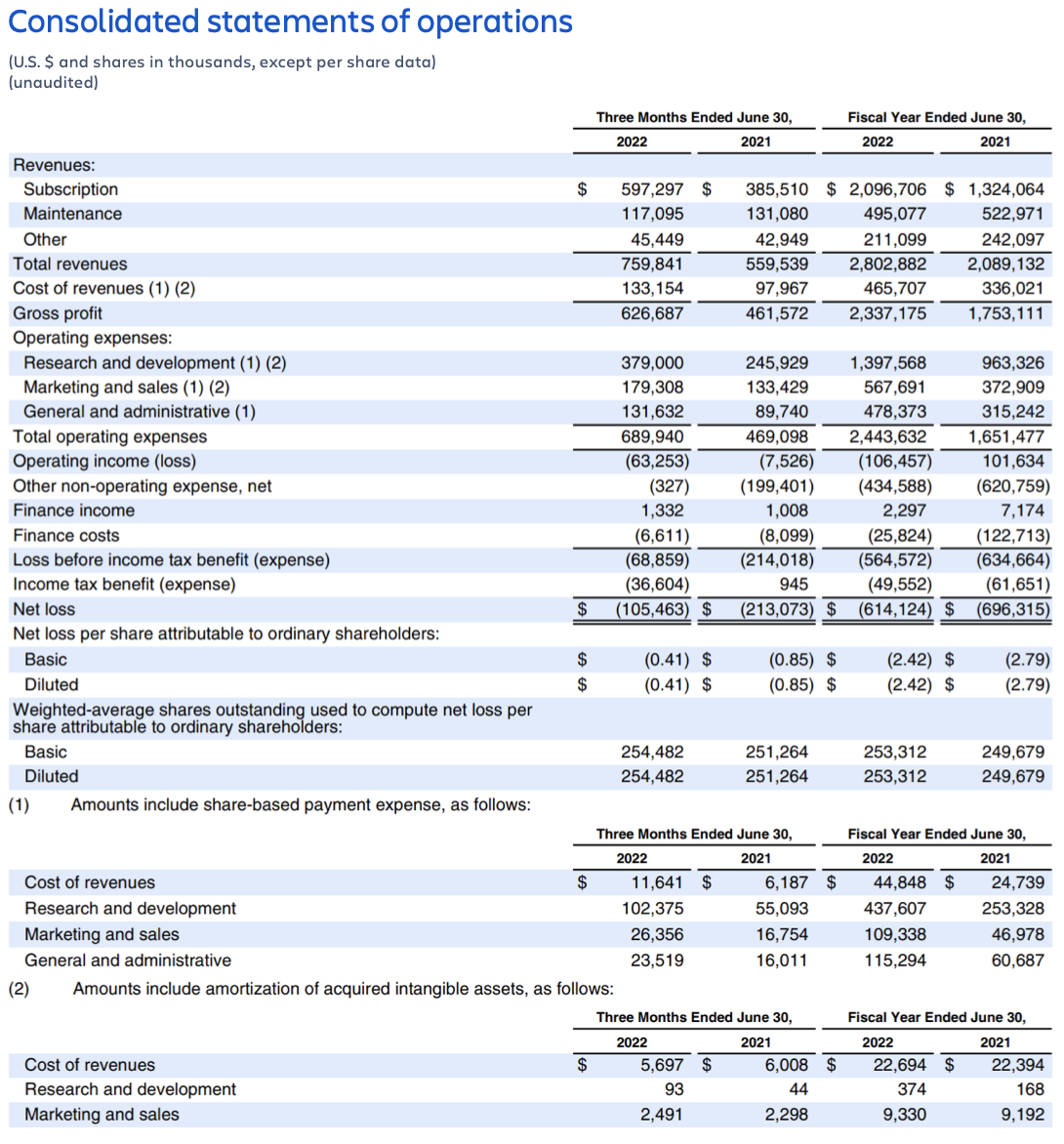

- Subscription revenue grew by 55% year-over-year. Cloud revenue grew by 55% year-over-year and Data Center revenue grew by 60% year-over-year. We are proud of these growth rates as we closed out FY22 in strong fashion.

- Cloud revenue continued to see durable year-over-year growth, against a tough compare.

- Data Center continued to see strong demand, driven in part by tailwinds from some customers purchasing ahead of pricing changes and the reduction of loyalty discounts.

- One of the things we’re most proud of is we continue to execute well against our ambitious hiring plans. We added 634 net new Atlassians in Q4’22, and over 2,300 net new Atlassians in FY22, bringing our total headcount to 8,813. Most of our new hires are focused on R&D. We will leverage our unique culture, “TEAM Anywhere,” and our financial capacity to continue adding top-tier talent in FY23.

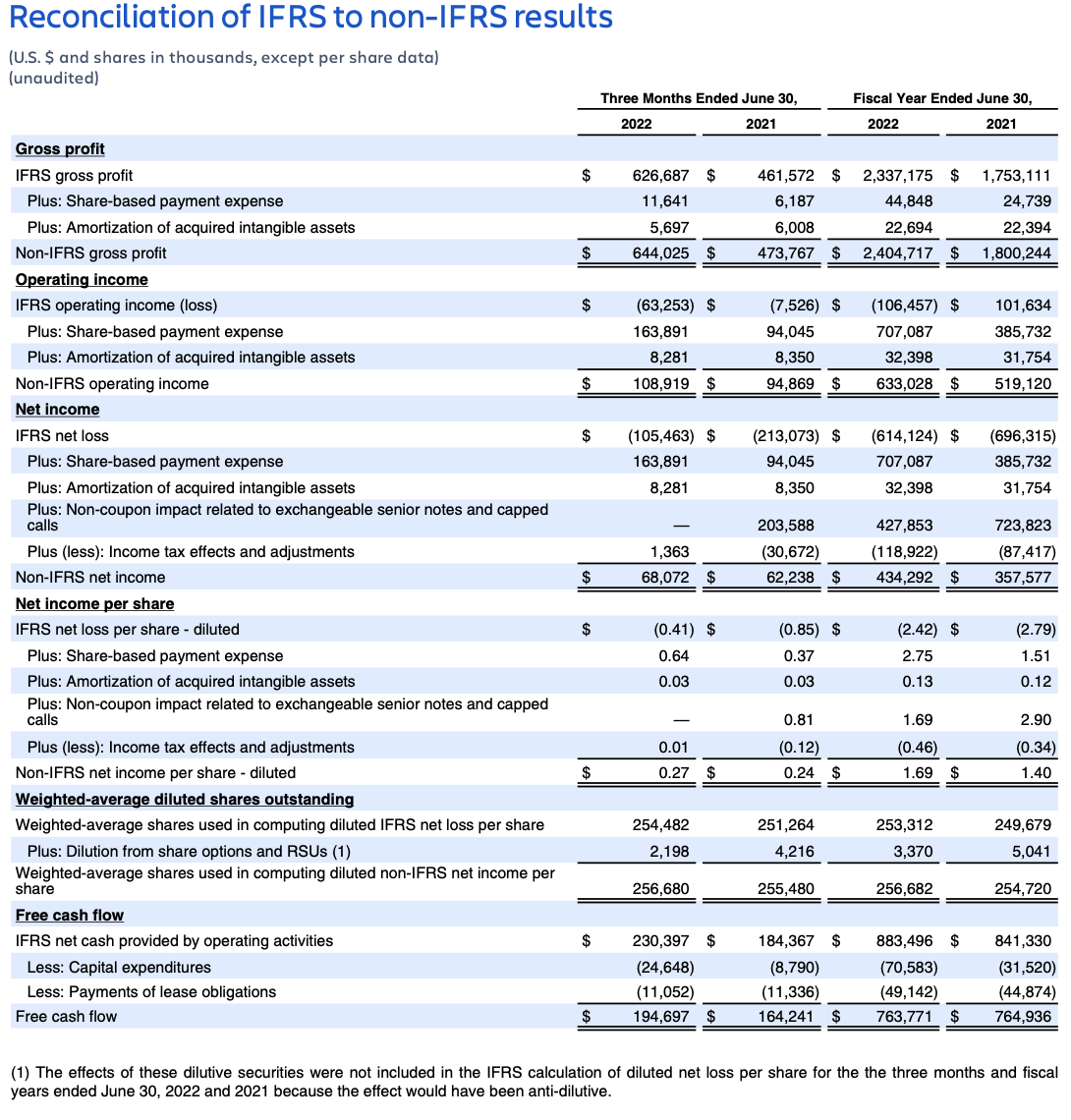

- We capped off FY22 with strong free cash flow results, even as we continue to invest against the sizable market opportunities in front of us. Free cash flow for Q4’22 totaled $194.7 million, representing a 26% free cash flow margin. Our strong financial position provides us with the flexibility to invest purposefully and create value for our customers.

Q4’22 operating margin was impacted by approximately one percentage point due to one-time costs we incurred as we supported a small cohort of customers through an outage in April 2022, fully restored their instances, and made improvements to enhance our internal processes.

Headcount

Total employee headcount was 8,813 at the end of Q4’22, an increase of 634 employees since the end of Q3’22. The majority of the increase was in R&D.

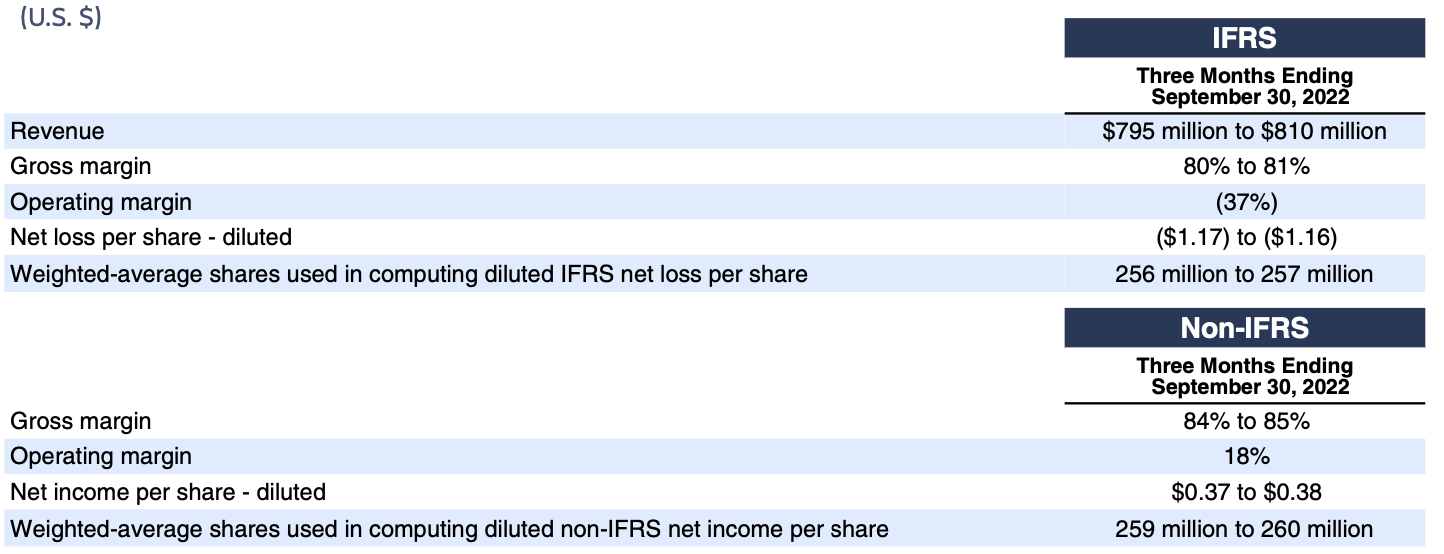

Fiscal 2023 outlook

Revenue

We continue to be pleased with the pace of our cloud migrations, and as we’ve previously stated, we have a multi-year migration journey ahead of us.

As a reminder, while we have discontinued sales of new Server licenses in Q3’21, as well as upgrades of existing Server licenses in Q3’22, we will continue to offer maintenance and support to Server customers until February 2024.

As a result, we continue to expect variability in our revenue growth quarter-to-quarter as Server customers choose the timing of when to migrate to our Cloud or Data Center offerings. We believe this variability will be transitory as we progress through the end-of-life date of Server in February 2024.

We were pleased with our Q4’22 results, which give us strong momentum going into FY23 and confidence to reaffirm our Cloud revenue growth targets of approximately 50% for the next two years. As mentioned earlier, we are not insulated from broader macroeconomic impacts. We are seeing a modest decrease in the conversion rates of Free instances upgrading to paid plans, but nothing we are seeing right now is changing our outlook. As a reminder, over 90% of our revenue in FY22 was derived from existing customers, and this dynamic has been consistent in our business over the years. We will remain vigilant and continue to inspect all aspects of our business relying on our well refined analytics and understanding of our funnels.

As we navigate this environment, we will continue our focus on delivering long-term value to customers. This focus has underpinned our business model and growth over the past 20 years, and will continue to drive our business going forward.

In FY23, we expect to see the following trends:

Subscription revenue

- Cloud revenue

- We are reiterating our expectations that Cloud revenue growth will be approximately 50% year-over-year for both FY23 and FY24, with approximately 10 points of this growth driven by migrations in both years.

- Cloud revenue will continue to be the primary driver of revenue growth.

- We expect our Cloud revenue growth to be relatively consistent over the course of FY23.

- Data Center revenue

- We saw strong Data Center revenue growth in FY22, benefited in part by event-driven demand resulting from customers purchasing ahead of price increases that went into effect during Q3’22 and the reduction of loyalty discounts at the start of Q1’23.

- For Data Center revenue, a portion is recognized up-front in subscription revenue in the period that the subscription begins, while the remainder is recognized ratably over the life of the contract.

- We expect Data Center revenue to maintain a high growth rate in Q1’23, before moderating over the remaining three quarters of FY23.

Maintenance revenue

- We expect maintenance revenue to continue to slowly contract over the course of FY23. In Q4’23, we expect maintenance revenue to decline to approximately $75 million.

Other revenue

- We expect other revenue to be approximately flat to slightly down relative to FY22.

- We do not expect any further perpetual license revenue in FY23. Perpetual license revenue, which was recognized in other revenue, totaled approximately $30 million in FY22.

- Marketplace revenue, which is reflected in other revenue, will continue to be impacted by the ongoing mix shift of the sale of third-party apps for Server and Data Center to Cloud. Sales of third-party Cloud apps have a lower Marketplace take rate relative to Server and Data Center, which is designed to incentivize further cloud app development.

- Our focus remains on driving a growth rate on sales of third-party Cloud apps greater than that of our own products. In FY22, we executed well on this goal, as gross sales of third-party Cloud apps in the Marketplace grew over 10 percentage points faster than sales of our own Cloud products.

- Marketplace revenue growth year-over-year will see a slight headwind because of the Data Center and Server event-driven app purchasing, that was primarily driven by pricing changes, that occurred in FY22.

- As a reminder, revenue on the sale of third-party Marketplace apps is recognized in the period the product is purchased.

Profitability

We continued to execute well on our plans to invest against our large market opportunities. We exit FY22 having hired 2,300+ net new Atlassians, advanced our platform, rolled out new features to existing Cloud products, and continued to innovate with new product offerings. Yet as we look forward, we see many significant opportunities as we continue to migrate customers to Cloud, as well as across agile & DevOps, ITSM, and work management.

In FY23, we will continue to invest purposefully to drive long-term durable growth. We will continue to hire talent from across the globe, primarily in R&D.

We expect the following dynamics to impact our margins in FY23:

- Gross margin will decrease modestly in FY23, due to the continued business mix shift to Cloud. This impact will be primarily driven by increased hosting costs for Cloud customers, as well as additional personnel costs to support cloud migrations and our Cloud customer base. We expect gross margins to be lower in the second half than in the first half.

- Operating margin will be in the mid-teens % in FY23 as we ramp our pace of hiring, focusing primarily in R&D, to seize on the opportunities in front of us. We expect operating margins to be lower in the second half than in the first half.

- Free cash flow is expected to be impacted as a result of the reduction in operating margin in FY23. Additionally, free cash flow may be impacted as a result of the continued business mix shift to the Cloud. Maintenance contracts for our Server products and subscription contracts for our Data Center products are only offered on annual terms, while we offer subscriptions for our Cloud products on both annual and monthly terms. In the short term, the shift to the Cloud and the potential mix change in billing terms may create a headwind for free cash flow. Over the long term, as more enterprise customers migrate to Cloud, we expect any such headwind to subside.

- As a reminder, our free cash flow results see seasonality quarter-to-quarter. Q1 is historically our lowest free cash flow margin result in a fiscal year, due to when employee bonuses are paid out. In FY23, we expect the timing of certain income tax payments to shift from Q2 to Q1, adding additional seasonality.

Share count

In FY23, we expect to see a meaningful increase in our share-based compensation (SBC) expense as we continue to play offense and invest in our team. Recall that we report our financial statements in accordance with IFRS. SBC is recognized on a front-loaded schedule compared to U.S. GAAP. We are forecasting approximately 2% share count dilution under IFRS for FY23.

Redomiciling from the United Kingdom to the United States

Previously, we shared that we are exploring redomiciling our parent holding company from the United Kingdom to the United States. Since then, our Board of Directors has approved the redomiciliation, and we will be seeking shareholder approval of the redomiciliation at two special meetings of the shareholders to be held on August 22, 2022. If Atlassian’s shareholders approve the redomiciliation, it is expected to become effective on September 30, 2022.

As a reminder, we believe moving our parent entity to the United States will increase our access to a broader set of investors, support inclusion in additional stock indices, improve financial reporting comparability with our industry peers, streamline our corporate structure, and provide more flexibility in accessing capital.

If the transaction is approved by our shareholders, we will transition our accounting standards from IFRS to U.S. GAAP (GAAP) beginning in Q1’23. We expect the following areas will be affected:

- Share-based compensation – GAAP utilizes “straight-line” ratable expense recognition instead of “graded” front-loaded expense recognition as currently done under IFRS. This change would result in pushing out our currently front-loaded expense recognition of SBC to later years, particularly as we continue to increase employee headcount.

- Leases – Under GAAP, we will likely see a slight expense delay to later periods.

- Strategic investments – Under GAAP, we will be required to record the quarterly mark-to-market fair value movements of our equity investments on our Consolidated Statements of Operations, while under IFRS, this is not required. This change would introduce quarterly fluctuations on our Consolidated Statements of Operations (other non-operating expense, net).

- Exchangeable senior notes – The amortization of the debt discount and issuance costs relating to our exchangeable senior notes, which were fully settled in Q2’22, follow different timing recognition rules under GAAP. This difference will result in a portion of amortization shifting from FY21 to FY22.

- Income tax accounting – This will be affected by the above accounting changes, in addition to various tax-specific guidance, including the requirements and methodologies for deferred taxes recognition, valuation allowances, and annual effective tax rate calculations.

The above areas will have no impact to revenue and an immaterial impact to free cash flow.

If the redomiciliation is approved by our shareholders, shortly after the effective date of September 30, 2022 we will furnish supplementary financial data that summarizes key financial metrics and results for FY21 and FY22 under GAAP.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. All statements other than statements of historical fact could be deemed forward looking, including risks and uncertainties related to statements about our products, customers, anticipated growth, infrastructure, platform, proposed redomiciliation, outlook, technology and other key strategic areas, and our financial targets such as revenue, share count, and IFRS and non-IFRS financial measures including gross margin, operating margin, and net income (loss) per diluted share.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission from time to time, including the section titled “Risk Factors” in our most recent Forms 20-F and 6-K (reporting our quarterly results). These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

ABOUT NON-IFRS FINANCIAL MEASURES

Our reported results and financial targets include certain non-IFRS financial measures, including non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow. Management believes that the use of these non-IFRS financial measures provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of our results of operations, and also facilitates comparisons with peer companies, many of which use similar non-IFRS or non-GAAP financial measures to supplement their IFRS or GAAP results. Non-IFRS results are presented for supplemental informational purposes only to aid in understanding our results of operations. The non-IFRS results should not be considered a substitute for financial information presented in accordance with IFRS, and may be different from non-IFRS or non- GAAP measures used by other companies.

Our non-IFRS financial measures include:

- Non-IFRS gross profit. Excludes expenses related to share-based compensation and amortization of acquired intangible assets.

- Non-IFRS operating income. Excludes expenses related to share-based compensation and amortization of acquired intangible assets.

- Non-IFRS net income and non-IFRS net income per diluted share. Excludes expenses related to share-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and a discrete tax impact resulting from a non-recurring transaction.

- Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment and payments of lease obligations.

Our non-IFRS financial measures reflect adjustments based on the items below:

- Share-based compensation.

- Amortization of acquired intangible assets.

- Non-coupon impact related to exchangeable senior notes and capped calls:

- Amortization of notes discount and issuance costs.

- Mark to fair value of the exchangeable senior notes exchange feature.

- Mark to fair value of the related capped call transactions.

- Net loss on settlements of exchangeable senior notes and capped call transactions.

- The related income tax effects on these items, and a discrete tax impact resulting from a non-recurring transaction.

- Purchases of property and equipment and payments of lease obligations.

We exclude expenses related to share-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and a discrete tax impact resulting from a non-recurring transaction from certain of our non-IFRS financial measures as we believe this helps investors understand our operational performance. In addition, share-based compensation expense can be difficult to predict and varies from period to period and company to company due to differing valuation methodologies, subjective assumptions, and the variety of equity instruments, as well as changes in stock price. Management believes that providing non-IFRS financial measures that exclude share-based compensation expense, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and a discrete tax impact resulting from a non-recurring transaction allow for more meaningful comparisons between our results of operations from period to period.

Management considers free cash flow to be a liquidity measure that provides useful information to management and investors about the amount of cash generated by our business that can be used for strategic opportunities, including investing in our business, making strategic acquisitions, and strengthening our statement of financial position.

Management uses non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow:

- As measures of operating performance, because these financial measures do not include the impact of items not directly resulting from our core operations.

- For planning purposes, including the preparation of our annual operating budget.

- To allocate resources to enhance the financial performance of our business.

- To evaluate the effectiveness of our business strategies.

- In communications with our Board of Directors and investors concerning our financial performance.

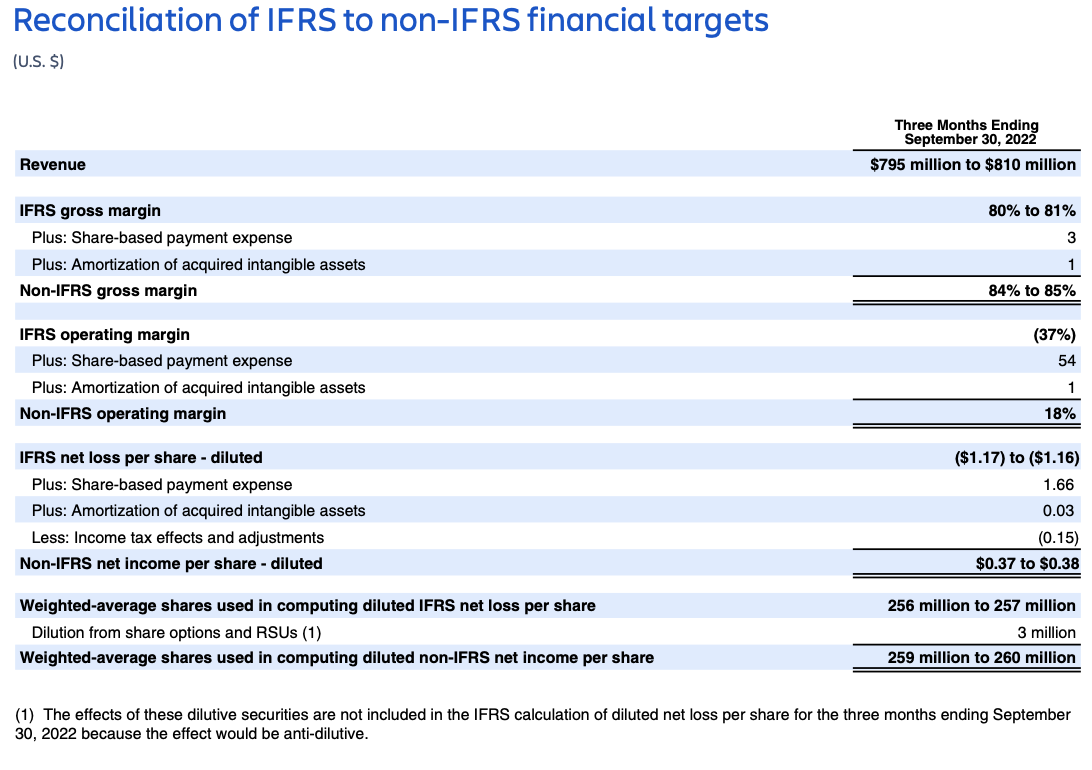

The tables in this shareholder letter titled “Reconciliation of IFRS to non-IFRS Results” and “Reconciliation of IFRS to non-IFRS financial targets” provide reconciliations of non-IFRS financial measures to the most recent directly comparable financial measures calculated and presented in accordance with IFRS. We understand that although non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow are frequently used by investors and securities analysts in their evaluation of companies, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results of operations as reported under IFRS.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our team collaboration and productivity software helps teams organize, discuss and complete shared work. Teams at more than 225,000 customers, across large and small organizations – including Redfin, NASA, Verizon, and Dropbox – use Atlassian’s project tracking, content creation and sharing, and service management products to work better together and deliver quality results on time. Learn more about our products, including Jira Software, Confluence, Jira Service Management, Trello, Bitbucket, and Jira Align at https://atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com

Media contact: Marie-Claire Maple, press@atlassian.com