Fellow shareholders,

We knew we’d be putting in the hard yakka 🇦🇺 this year, and that’s exactly what we’ve done. Atlassian ended FY23 with over 260,000 total customers and generated over $3.5 billion in revenue in the face of a challenging economy. And importantly, our three biggest bets are paying off, further strengthening our conviction in our strategy.

- Cloud – 250,000 customers now power collaboration using our world-class cloud platform. And we’re delivering more platform innovations and enhancements to our 14 integrated products every quarter. Millions of users migrated from Server and Data Center to our Cloud offerings in FY23, drawn by the incredible customer experience we’ve been building.

- Enterprise – Driven by platform updates such as support for 50,000-user instances, and bolstered by a robust network of partners and dedicated customer success teams, enterprises are deepening their commitment to Atlassian. Sales to enterprise customers grew over 50% year-over-year in FY23, all on the back of our best-in-class GTM efficiency.

- ITSM – We’re delivering the sophisticated capabilities IT teams need, along with features tailored to support teams like Legal and HR, at an unparalleled value. Over 45,000 customers now use Jira Service Management, and we’re seeing increased demand from enterprise customers with cloud sales to this segment up 80% year-over-year in FY23.

We also took advantage of mind-blowing developments in AI to bring generative capabilities into our products and unleash even more of our customers’ potential. And we responded to a rapidly shifting environment by rebalancing our teams so we can meet our customers’ needs faster.

In other words, we did what we said we were going to do: play offense.

There are massive opportunities in cloud, enterprise, and ITSM that will drive Atlassian’s growth for years to come. Plus, tech’s labor market is such right now that we’re able to hire amazing talent who might not otherwise be available.

These moves set Atlassian up to win over the long term and reflect our enduring confidence in our business model, our strategy, and our team. We aren’t afraid to make tough tradeoffs in support of durable growth that others shy away from, even when it may be uncomfortable in the short term.

This is consistent with the strategy we communicated to you at our Investor Day in April 2022. It was there that we also committed to returning to historical operating margins. That hasn’t changed. Starting in FY25, we expect operating margins to expand from the FY24 guidance we’re providing today and begin trending towards the historical margins Atlassian is known for, driven by durable revenue growth combined with moderating investment in areas we’ve accelerated over the past two years, like cloud migrations.

Our job in this next year is to keep the momentum high on cloud migrations and continue delivering differentiated value across our three markets. Execute on the massive opportunities in front of us and we’ll exit FY24 in an even stronger position.

Looking toward the next leg of our cloud journey ⛅️

Atlassian generated over $2 billion in cloud revenue and migrated millions of users to the cloud in FY23. The cloud-only offerings we launched in FY23, like Jira Product Discovery and Beacon, are resonating with customers, and Atlassian Analytics is proving to be especially compelling to our enterprise customers. We know we’re on the right track, and we’re not looking back.

We beat our migration goals for Q4, as well as resolved major barriers to migration around data residency, user management, and backup capabilities. Becoming a cloud-first company has been our top priority in recent years. As a result, over 250,000 Atlassian customers now use at least one of our Cloud products. Or, in the case of Roblox, a half dozen of them.

Noticing the high caliber of our cloud-only offerings, Roblox, a wildly popular online gaming platform, knew it was the perfect time to move off Data Center, as well as replace their legacy ITSM tool with Jira Service Management. Now they benefit from cloud-only offerings like virtual agents for AI-driven service management, Beacon for threat detection, and cross-product smart links that keep it all connected.

Before, our team saw Atlassian as individual tools…Now, [features and integrations] like macros and Smart Links have really been pivotal in collaboration, productivity, and discoverability.

– Joe Cotant, Sr. Technical Program Manager at Roblox

Migrations will continue to be an important lever of growth for us beyond FY24, particularly with our enterprise customers. In speaking with them, it’s clear the cloud is their ultimate destination. We’ve already made great strides here, with Data Center customers accounting for approximately 50% of migrations to Cloud. So we’re putting even more energy into offering instances beyond 50,000 seats, as well as delivering on their data governance requirements, supporting their extensibility needs, and working on capabilities tailored to enterprises.

But wait! There’s more.

We shipped another batch of enhancements to the Atlassian platform that unlock ![]() our Cloud products for millions more user seats, as well as crowd-pleasers

our Cloud products for millions more user seats, as well as crowd-pleasers ![]() that keep customers coming back. Here’s a sample.

that keep customers coming back. Here’s a sample.

“BYO key” encryption option for Jira and Jira Service Management (Early Access)

“BYO key” encryption option for Jira and Jira Service Management (Early Access)- Data residency option in Singapore

- Data residency options for 3rd-party Connect apps

- “User access” admin role for managing access to specific products

- Improved backup and restore capabilities (Early Access)

- Invalid and duplicate user detection in migration tooling

Dark theme in all Jira products for reduced eye strain

Dark theme in all Jira products for reduced eye strain- Updated portal sign-up flow that reduces friction

- Faster editor performance in Confluence

- Multi-project visualization tools in Jira Work Management for cross-team collaboration

You can’t spell “Atlassian” without “AI”

Whilst AI is great, AI plus data is where the real value lies. This gives Atlassian a huge advantage. With two decades’ worth of insights about teamwork, and the data customers store across our products (including long-form text from Confluence), we can enhance generic AI answers with contextual information on a per-customer basis. The result is exceptionally useful output, tailored to each customer’s unique knowledge base and organizational structures.

So when generative AI exploded onto the scene this year, we seized the moment and rolled out a new “virtual teammate” for our customers that we call Atlassian Intelligence.

Generative AI is poised to expand Atlassian’s opportunities in a big way. In the near term, customers are considering fast-tracking their moves to the cloud so they can take advantage of these powerful capabilities. And as the high-value, high-volume leader, we’re building differentiated levels of AI capabilities across our Cloud editions, as a way to attract new customers and give existing customers compelling reasons to upgrade.

Beyond these nearer-term opportunities, we see the potential for more Atlassian users over the long term. AI will enable more people to create software, which is currently supply constrained. More creators means more collaboration needs, as well as more teams to build, deploy, and sell this technology.

The year in review across our three global markets 📆

Atlassian products solve five primary teamwork challenges for our customers: tracking work; sharing knowledge; getting help; creating high-performance teams; and doing it all at scale. But no single product can cover all five jobs for every team across the three global markets we serve. Our approach is to offer a range of purpose-built, fully-integrated tools so customers can curate a collection that best suits their needs.

Empowering customers with this choice as well as focusing on robust integrations with best-of-breed partners helps Atlassian win across the ITSM, work management, and agile/DevOps markets we serve. Let’s look at highlights from all three and show how we helped customers thrive this year.

We advanced our position in the ITSM market this year, focusing on bringing development and IT teams closer together, while also helping a wider range of non-technical teams deliver great employee support. We were named a Leader in the 2022 Gartner® Magic Quadrant™ for IT Service Management Platforms1. We also grew cloud sales to enterprise customers by 80% year-over-year – proof that doubling down on ITSM was the right call.

Some of the highest-value updates we shipped to our 45,000+ Jira Service Management customers include:

- New CI/CD integrations with GitHub and GitLab that automate change approvals

- Cross-product insights via Atlassian Analytics that correlate incidents and changes

- Device42 and Lansweeper integrations for easier incident and change impact analysis

- Virtual agent technology powered by Atlassian Intelligence (Early Access)

- Chat-based ticketing so employees can get help right from Slack and Microsoft Teams

- Employee support templates that help teams like Finance, Marketing, Design, and Sales deliver service faster

- Support for up to 20,000 agents per instance (Early Access)

Atlassian is the only vendor that brings technical and non-technical teams together on the same platform, yet lets them work with tools that are designed for their respective crafts. We’ll continue to build on the existing trust we have with development teams to expand into more IT departments (and beyond) so their teams can deliver what would be impossible alone: exceptional service. ![]()

Atlassian delivered new forms of collaboration this year, like the ability to structure and visualize information differently with databases and whiteboards in Confluence. We also launched Atlas into general availability, giving teams of all types better ways to manage projects and ensure they contribute to the organization’s most important goals. Jira Work Management added a Premium edition, which includes multi-project summaries, timelines, and calendars so leaders can get a holistic view of all the work they manage. And to top it all off, Confluence made the top five in G2’s Best Software for Enterprise Business list for 2023. 🏆

The non-technical teams market, which we estimate at $14 billion, represents a huge opportunity. Atlassian unites technical and non-technical teams through the common language of our Jira products and the connective tissue of our integrated cloud platform. No other vendor can match this, so we’ll keep leaning in hard here.

For software teams, Jira is still the GOAT ![]() and developer experience remains a priority for Atlassian. As such, we created a Security tab in Jira that brings DevSecOps into all aspects of software development by turning alerts from leading security vendors (e.g., Snyk, Mend, Lacework, Stackhawk, JFrog) into issues, making it easy to track remediation work. And we rolled out a dark theme for Jira’s UI, satisfying a popular enhancement request.

and developer experience remains a priority for Atlassian. As such, we created a Security tab in Jira that brings DevSecOps into all aspects of software development by turning alerts from leading security vendors (e.g., Snyk, Mend, Lacework, Stackhawk, JFrog) into issues, making it easy to track remediation work. And we rolled out a dark theme for Jira’s UI, satisfying a popular enhancement request.

Atlassian is leading the charge in helping organizations master the complexity introduced by the shared microservices and myriad other components that comprise modern software. Not only did we get Compass into customers’ hands this year, but we also delivered configuration-as-code enhancements that help teams catalog and manage all the elements involved in distributed software architecture.

But creating software goes far beyond developers writing code. That’s why we launched Jira Product Discovery, which lets product managers capture and prioritize ideas. It’s also why we’re confident in our approach of connecting developers, designers, marketers, support engineers, and others. Atlassian’s Open DevOps framework allows for interoperability between Jira products and a variety of best-of-breed 3rd party tools. We believe being named a Leader in the 2023 Gartner® Magic Quadrant™ for DevOps Platforms2 is the type of recognition that lets us know we’ve got a winning strategy.

Team Anywhere: a win for employees and customers everywhere 🌏

Three years ago this month, we placed another big bet: we declared Atlassian a remote-first company. Whether all-remote or hybrid, distributed teams are the future of work. We’re committed to living that future now and pioneering solutions to the challenges of working across geographies and time zones. When we uncover valuable insights, we bake them into our products or share them with our customers through content.

Team Anywhere allows us to hire the best person for the job regardless of how close they live to one of our offices. In fact, over half of the people we hired in FY23 live more than two hours away from an office. As of Q4, we have full-time employees in 13 countries on four continents, spread across urban centers and rural areas. 91% of our employees say Team Anywhere is an important reason for staying at Atlassian, and 92% say it allows them to do their best work.

While some business leaders accuse us of abandoning something essential to our esprit de corps, we see it differently. We see a chance to lead. Atlassian is one of the only enterprise companies to go all-in on distributed work. Customers and peers are turning to us for advice, inspired by the example we’re setting.

To be clear, getting 10,000 distributed employees to sing in perfect harmony is no small feat. But with an average of 67% of the company connecting in an office each quarter and strong participation in our in-person “intentional togetherness” events, Atlassian is demonstrating that distributed work and deep connections between teammates can go hand-in-hand, even at this scale. The more we lean in here and lead the way, the deeper our competitive advantage.

With FY24 already underway and teams in full execution mode driving towards this year’s big goals, we feel pretty damn lucky. Not every entrepreneur makes it to the 10-year mark, even when they do all the right things, and here we are, 21 years into our Atlassian journey. (Not bad for a couple of mates from uni, if you ask us!) We’re more excited than ever about the opportunities in front of us and fired the F up to get after them.

A bittersweet farewell 💙

After almost 11 years of tireless leadership and dedication, Cameron Deatsch, our Chief Revenue Officer, has decided to leave Atlassian at the end of the calendar year for new life adventures.

Cameron has played a central role in helping our customers in their journey to cloud over the past several years and has had a tremendous impact in every area he’s overseen at Atlassian over his decade-plus tenure. From building out our customer-facing teams and evolving our GTM model, to leading our Server and Data Center product organizations, and even a stint as Head of Corporate Development – Cameron has seen and done it all. Equally important is the strong and experienced team he has built to continue that legacy.

We, the founders, and our entire Atlassian family will be forever thankful to Cameron for his inspirational leadership over the years. We are thankful for the huge impact he has had on our customers, our growth, and our culture. We will miss you, Cameron.

Here’s to the road ahead, and to unleashing the potential of every team.

– Mike and Scott

the bottom line

- Atlassian continued to deliver exceptional customer value and innovation in the face of a tough macroeconomic climate, closing out the year with over 260,000 customers and $3.5 billion in total revenue.

- Our biggest bets – cloud, enterprise, and ITSM – are paying off, as evidenced by strong momentum in all three areas.

- We’ll press ahead with our strategy of accelerated investment in FY24, and expect to begin trending towards historical operating margins in FY25.

Customer highlight reel 📽️

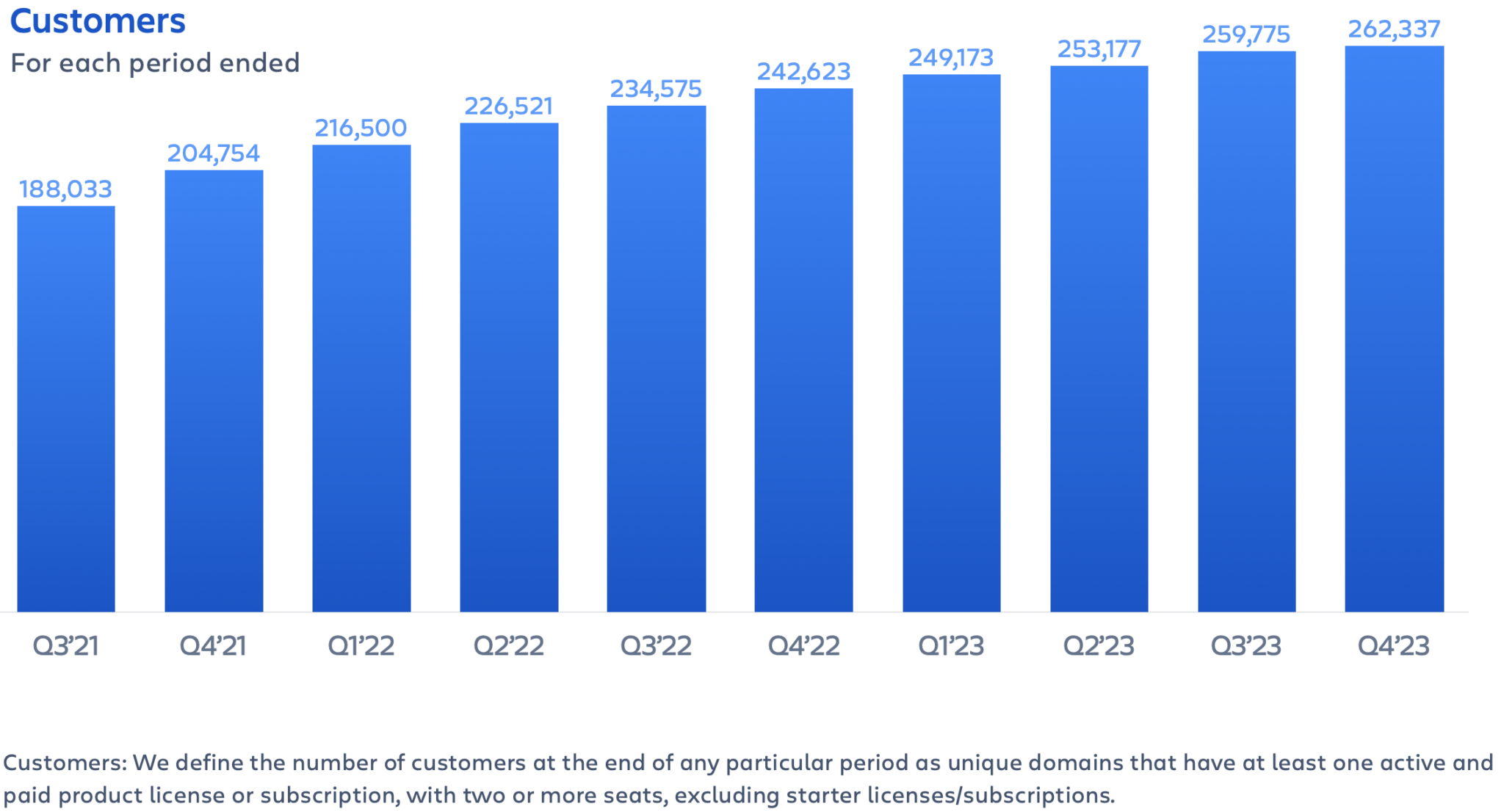

Despite the tough macro environment we encountered in FY23, Atlassian made steady progress against our long-term goals across our broad, diversified customer base. We closed out the fiscal year with 262,337 total customers – up nearly 20,000 over the prior fiscal year.

Net new customer additions for Q4 were 2,562.

Conversions from Free editions to paid products remain challenged by the macroeconomic environment. However, we continue to be encouraged by the activity at the top of our funnel, as the number of teams coming to our site and trying Free editions of our products continues to grow. And importantly, customer churn continues to be stable, as is usage across our products, reflecting the value and inherent demand for our products.

And as a result of the macroeconomic environment, we’ve had to make thoughtful tradeoffs this year, including consciously shifting marketing resources to prioritize growth in customers with the highest lifetime value. The great news is, we’re seeing this strategy pay off.

As a volume-based business, we aim to serve the “Fortune 500,000.” That’s what our flywheel-led GTM motion is designed for, and that’s not going to change. However, we’re constantly improving our enterprise capabilities and evolving the higher-touch motions that help us make deeper inroads with enterprise customers.

Our Cloud platform now meets some of the strictest compliance standards in the world (think EBA, BaFin, HIPAA), and as discussed earlier, we have our sights set on supporting well beyond 50,000 users. Marquee features like Atlassian Analytics and the Atlassian Data Lake are already prompting customers to upgrade to Premium and Enterprise editions. For example, H&M moved up to Enterprise this quarter so they could identify trends in their data and make sure their teams’ work aligns with strategy. Plus, data residency options in new regions like Germany and Singapore give enterprise customers even more confidence in the Atlassian platform.

Customer spotlight

Jira and Confluence have long been the life-blood of development at a major U.S. maker of high-end office furniture. (Chances are, you’re sitting in one of their ergonomic chairs right now.) But the cost and complexity of their monolithic legacy ITSM solution were dragging them down. They needed better coordination between their technical teams, and their CIO was keen to move to the cloud. So they switched to Jira Service Management.

Now with the combined power of all three products, they have a unified way of tracking projects, managing help requests, and sharing technical documentation. This is allowing them to move toward a decentralized support model where IT specialists are embedded in software teams to make incident and change management an integrated process shared across both disciplines. In fact, the switch to Jira Service Management has been so successful that non-technical service teams like HR have adopted it.

Looking ahead, the economic environment is still uncertain and on top of that, we’ve entered the final year of support for our Server products, which ends in February 2024. But the reality is, Atlassian is extremely well prepared to roll with the changes as they come and keep the momentum high as we come out the other side of the current downturn.

– Cameron

Financial highlights 📈

Q4’23 highlights

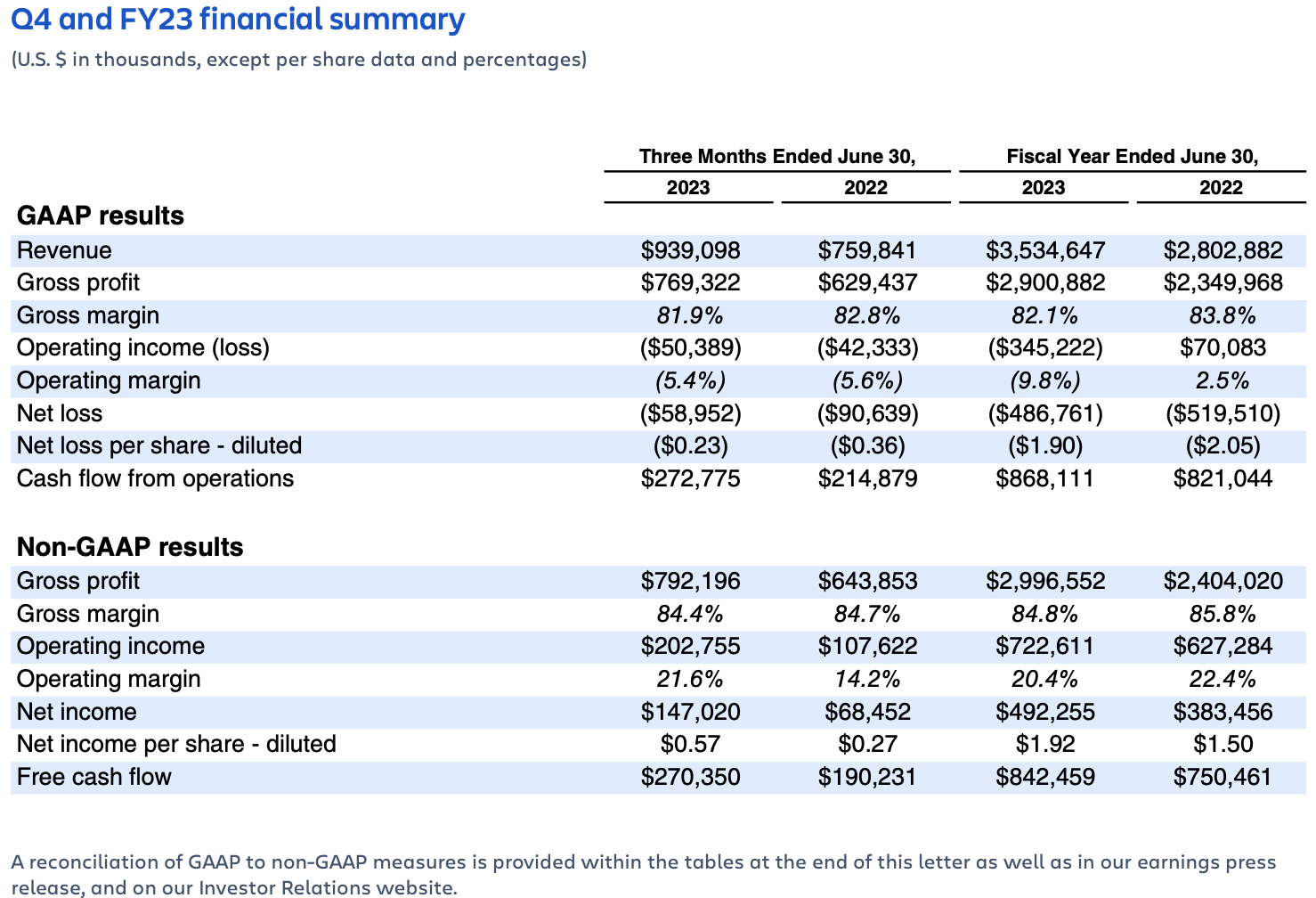

We closed out FY23 with strong execution, delivering revenue, gross profit, and operating income that exceeded our expectations.

Greater-than-expected enterprise sales driven by the expiration of our loyalty discount program and record migrations resulted in revenue outperformance in Cloud and Data Center, while gross profit and operating profit also benefited from our focus on disciplined hiring and cost management.

Guided by our mission of unleashing the potential of every team, we remain committed to delivering compelling value to our customers as we invest in our unique opportunities to drive long-term growth in FY24 and beyond.

Highlights for Q4’23 include:

All growth comparisons below relate to the corresponding period of last year, unless otherwise noted.

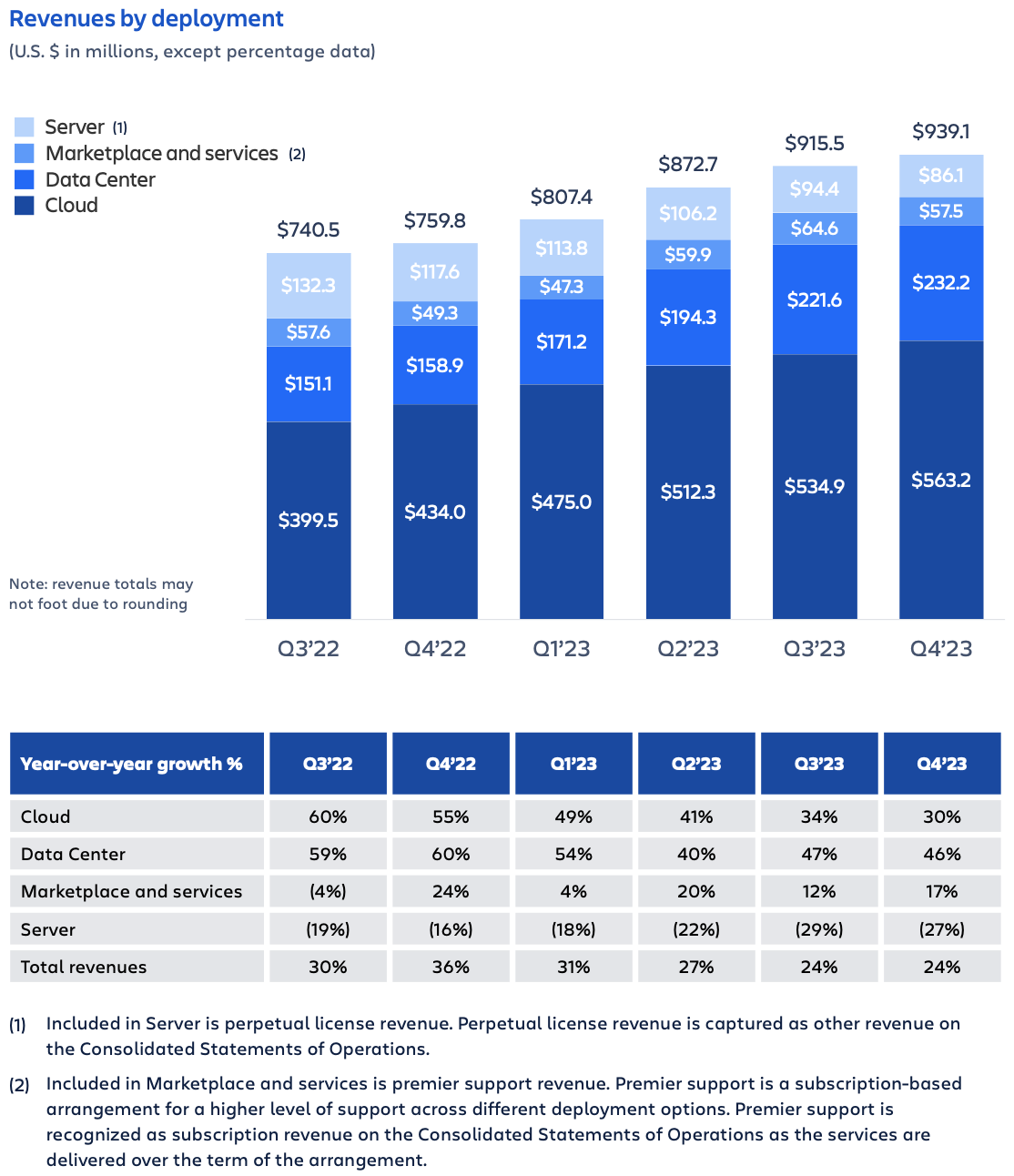

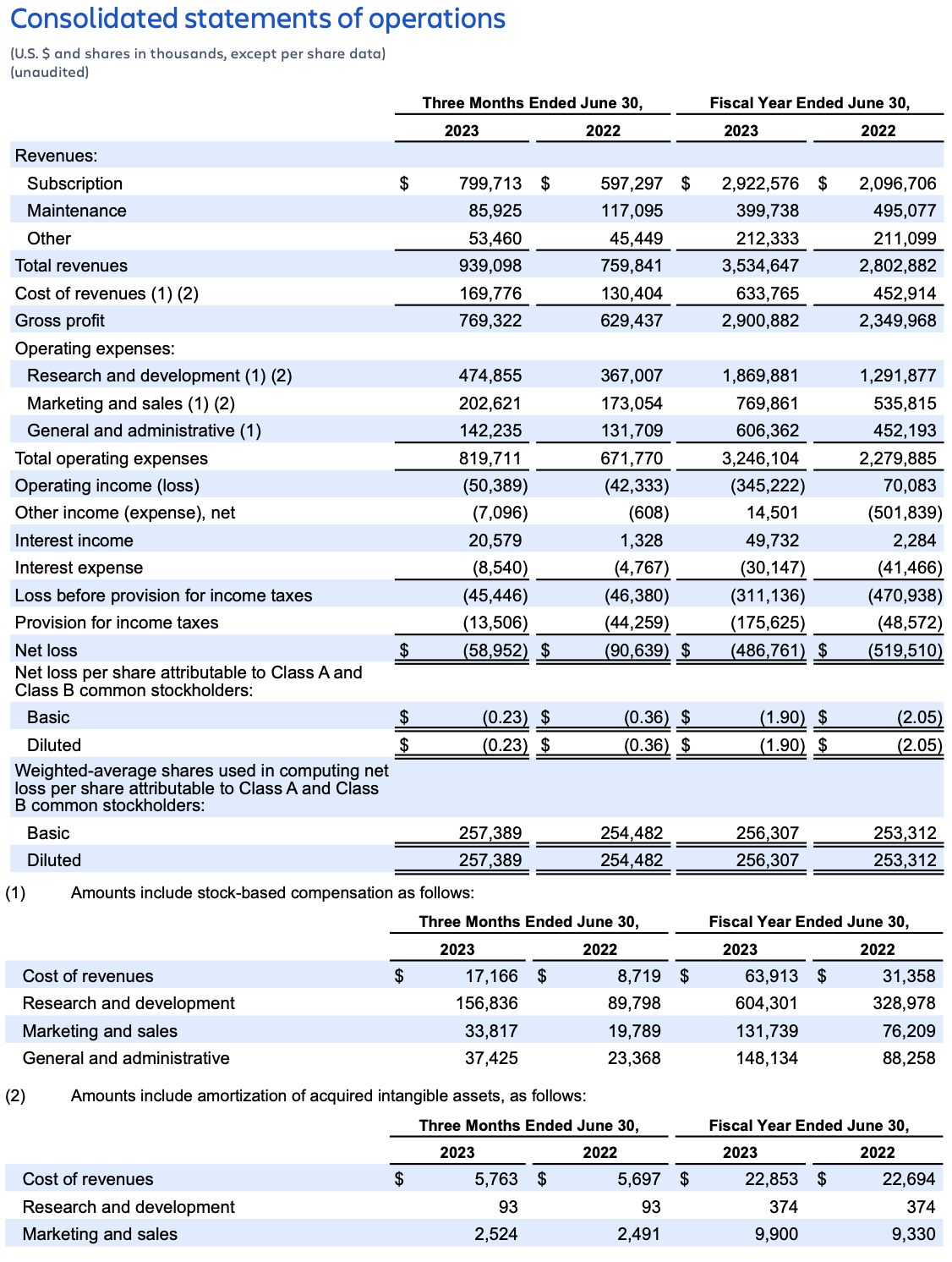

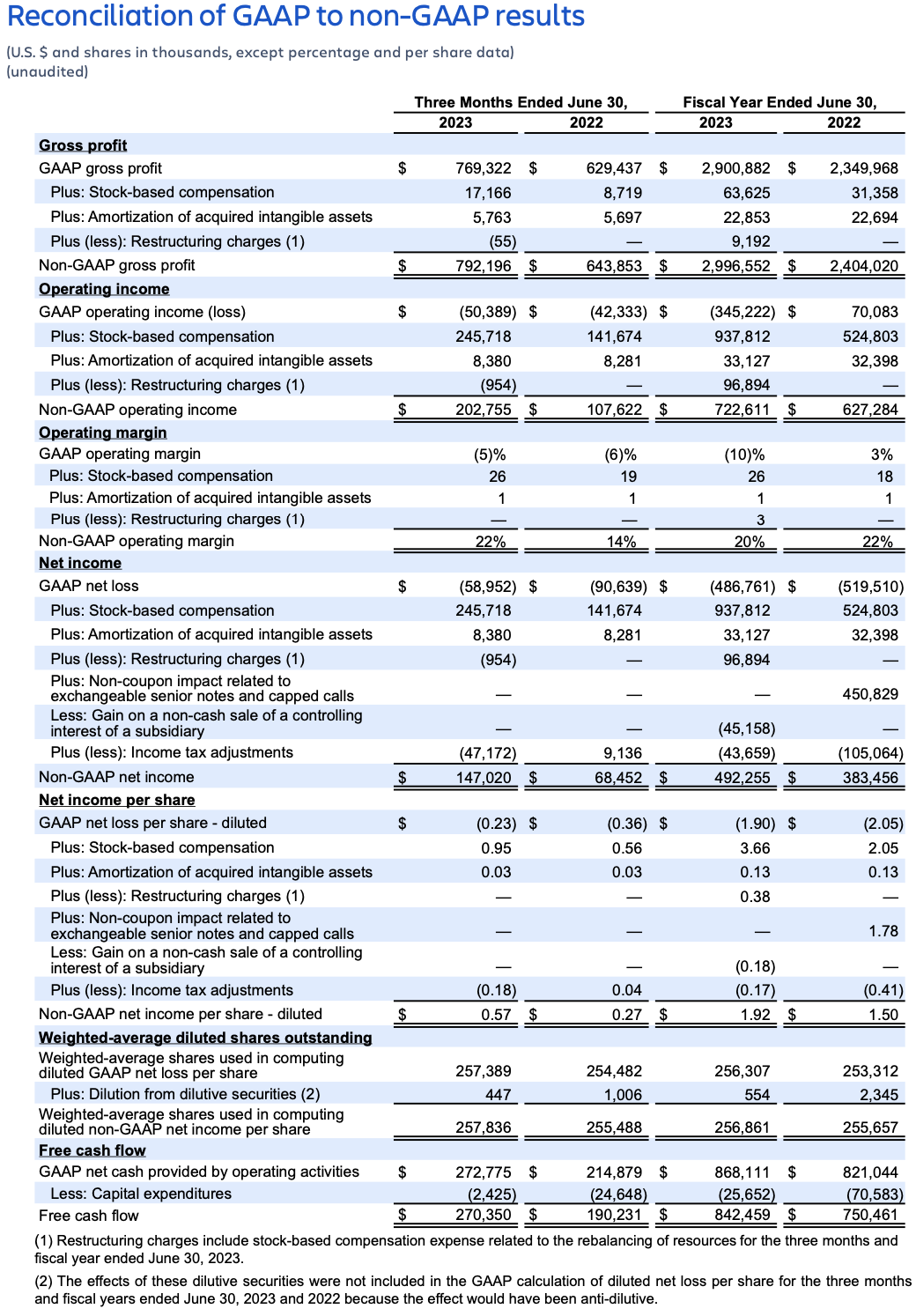

- Revenue of $939 million increased 24%, driven by growth in our Cloud and Data Center offerings.

- GAAP gross margin of 82% decreased 1 percentage point. Non-GAAP gross margin of 84% was flat.

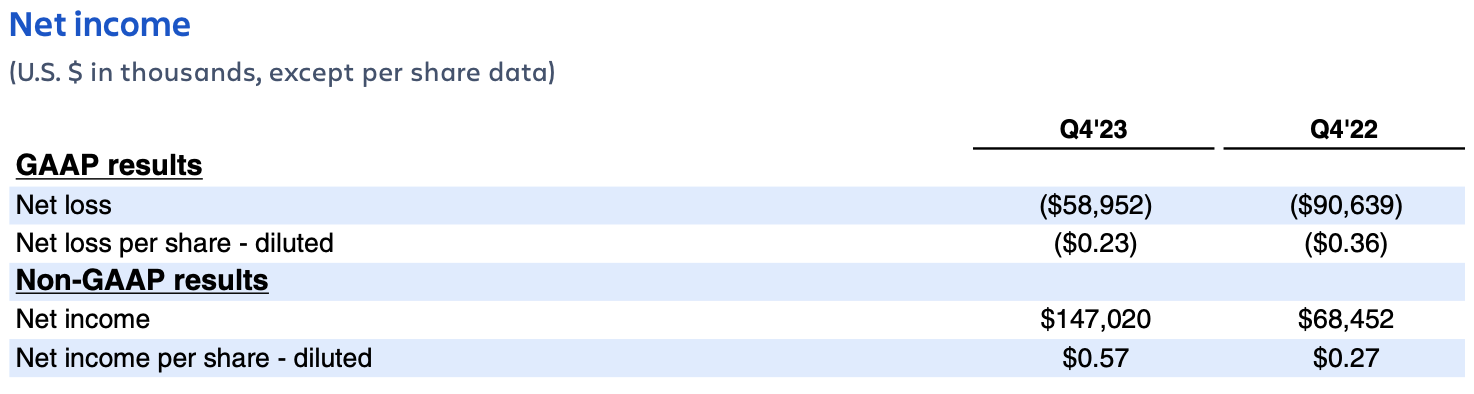

- GAAP operating loss was $50 million and GAAP operating margin of (5%) was flat. Non-GAAP operating income was $203 million and non-GAAP operating margin of 22% increased 8 percentage points driven by greater operating leverage.

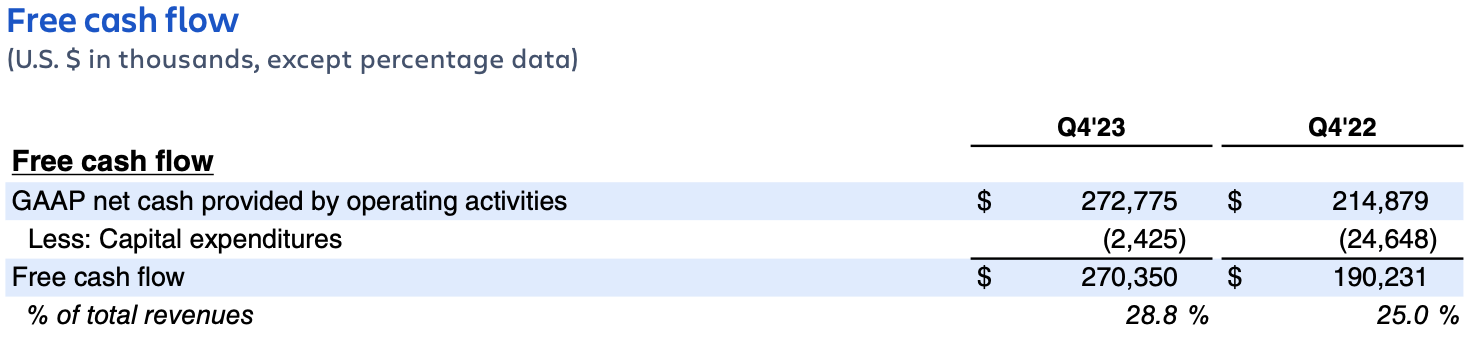

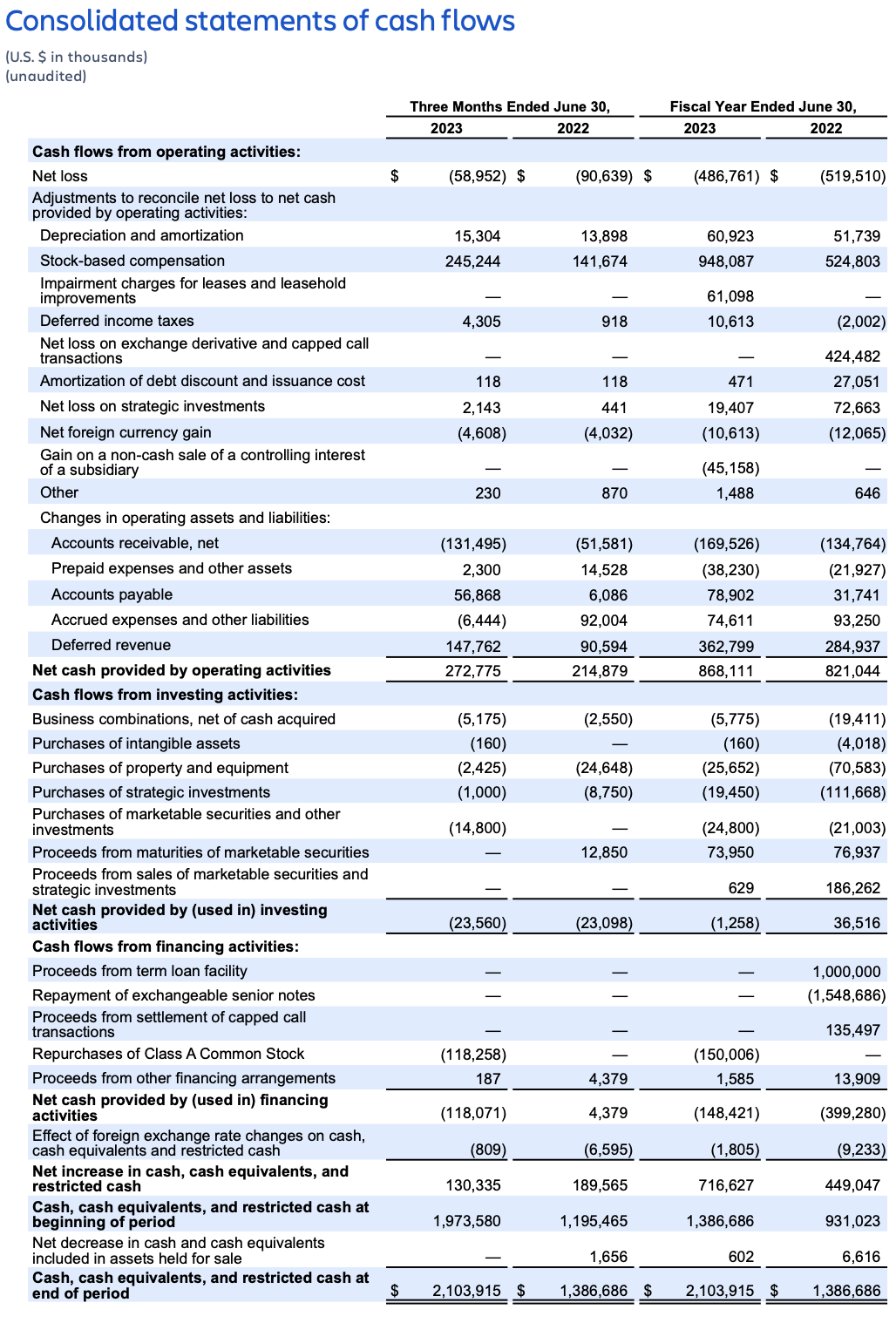

- Operating cash flow was $273 million. Free cash flow of $270 million increased 42%.

- Returned $118 million to shareholders through share repurchases in the quarter.

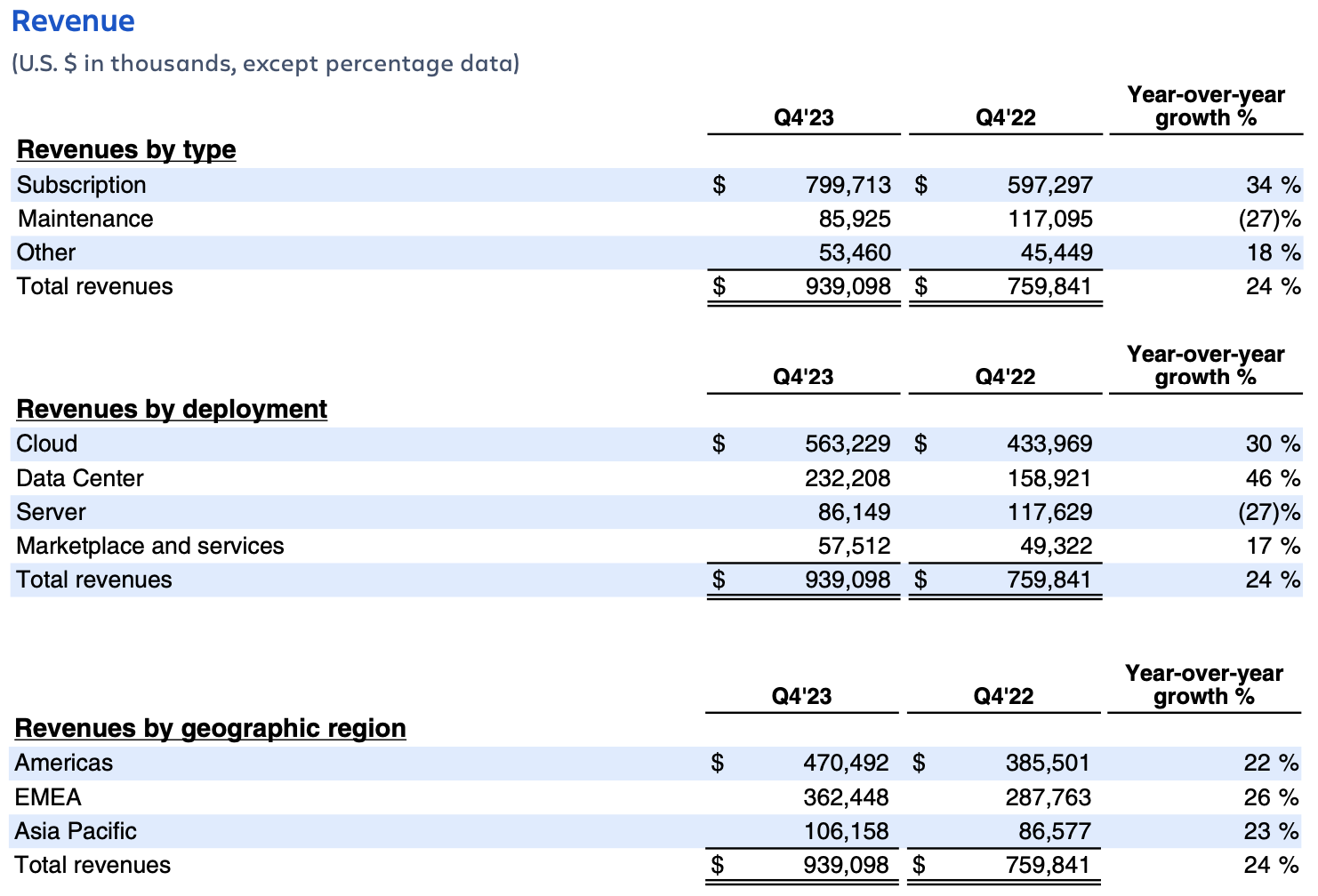

Revenue growth in Q4 was driven by subscription revenue, which grew 34%. Enterprise sales were particularly healthy with focused sales execution ahead of the end of our loyalty discount program on June 30, 2023. This drove record migrations to Cloud and Data Center, with strong uptake of Premium and Enterprise editions as well as annual and multi-year subscriptions.

Cloud revenue growth of 30% was better than expected driven primarily by stronger migrations and net seat expansion. The macro headwinds on paid seat expansion observed throughout FY23 persisted in Q4, however, the rate of deceleration began to moderate slightly towards the end of the quarter, particularly with enterprise customers. Free-to-paid conversion rates remain challenged, while customer retention and monthly active usage trends across the business remained stable as we continue to maintain our strong competitive position.

Data Center revenue growth of 46% was driven by renewals, migrations, and seat expansion, while also benefiting from the stronger-than-expected enterprise sales previously noted.

Lastly, deferred revenue increased 31% year-over-year to $1.5 billion reflecting strong growth in annual and multi-year subscriptions and customer commitment to the Atlassian platform.

GAAP operating expenses increased 22% year-over-year driven by higher employment costs, including stock-based compensation, due to the year-over-year increase in headcount.

Non-GAAP operating expenses increased 10% year-over-year and were lower than expected due primarily to payroll savings from lower headcount and greater-than-expected savings in discretionary spending.

GAAP operating margin of (5%) and non-GAAP operating margin of 22% benefited year-over-year from moderation in the pace of hiring, cost savings from our Q3’23 restructuring activities, lower bonus expense, and disciplined cost management and operating efficiencies across the business.

Free cash flow in Q4’23 was affected by $18 million of payments for employee severance and other termination benefits related to our Q3’23 restructuring activities.

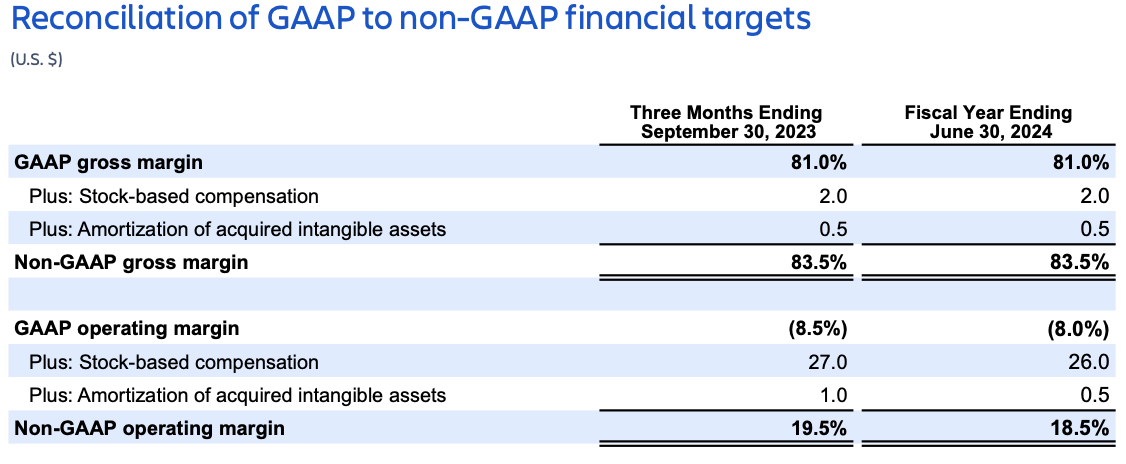

Financial targets (U.S. $)

FY24 outlook

Total revenue

While we are pleased with our momentum exiting FY23, our guidance accounts for two significant factors which may impact our revenue results in FY24.

The first is the outlook for the macroeconomic environment, which remains uncertain. Our guidance assumes the macroeconomic environment continues to negatively impact growth in paid seat expansion at existing customers and free-to-paid conversion rates, and that the trends we’ve seen in these areas throughout FY23 persist into FY24.

The second is customer purchasing and migration decisions related to the end-of-support for our Server offering in February 2024. We expect this event to drive quarter-to-quarter variability in our Cloud and Data Center revenue growth rates depending on when and how our Server customers ultimately choose to migrate: direct to Cloud, direct to Data Center, or to some combination of Cloud and Data Center. Our guidance assumes Server customer migration rates to Cloud and Data Center are consistent with historical trends, and some portion of our Server customers will not migrate in FY24. As a reminder, a portion of Data Center revenue is recognized up-front in the period the subscription begins, while the remainder is recognized ratably over the life of the subscription. Cloud revenue is recognized ratably over the life of the subscription.

Further detail and expected trends are provided below:

SUBSCRIPTION REVENUE

Cloud revenue

We expect Cloud revenue growth of approximately 25% to 30% year-over-year in FY24, of which migrations will drive approximately 10 points. We also expect Cloud revenue growth rates will gradually improve throughout the year driven by easier year-on-year comparisons.

Data Center revenue

We expect Data Center revenue growth of approximately 30% year-over-year in FY24, with growth decelerating over the course of the year primarily driven by tough year-on-year comparisons, declining migrations from Server, and increasing migrations to Cloud.

MAINTENANCE REVENUE

In line with our announced end-of-support for Server, we expect Server revenue to progressively decline throughout the course of FY24, with a sequential dollar decline in Q1’24 like that observed in Q4’23.

As a reminder, we will no longer recognize Server revenue beyond February 2024, and therefore expect Server revenue to be zero in Q4’24.

OTHER REVENUE

We expect Other revenue, which is primarily comprised of Marketplace revenue, to be roughly flat year-over-year in FY24 driven by the continued sales mix shift to Cloud apps.

As a reminder, there is a lower Marketplace take rate on third-party Cloud apps relative to Server and Data Center apps to incentivize further Cloud app development and Marketplace revenue is recognized in-full in the period of the Marketplace sale.

Our focus remains on driving higher growth rates on sales of third-party Cloud apps relative to our own first-party Cloud products, and in FY23 we accomplished this as gross sales of Cloud apps in the Marketplace grew 10 percentage points faster than sales of our own Cloud products.

Gross margin

We expect FY24 GAAP gross margin will be approximately 81.0% and non-GAAP gross margin will be approximately 83.5%, lower than FY23 due to the continued revenue mix shift to Cloud.

Operating and free cash flow margin

We expect FY24 GAAP operating margin will be approximately (8.0%) and non-GAAP operating margin will be approximately 18.5%. We expect operating expense growth will be driven by continued investment in key strategic priorities like cloud migrations, penetrating our enterprise opportunity, and delivering compelling innovation and customer value across our three core markets. These investments will drive long-term growth as we continue to execute on the multi- year strategy shared at our Investor Day in April 2022.

And, as Mike and Scott highlighted above, we remain committed to returning to historical margins following this period of accelerated investment, and we expect that to begin in FY25 with non- GAAP operating margin above the 18.5% we expect to achieve in FY24.

As a reminder, our free cash flow margins have quarter-to-quarter seasonality, with Q1 historically the lowest driven by the timing of employee bonus payouts.

Share count

We expect diluted share count to increase by less than 2% in FY24.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward looking, including risks and uncertainties related to statements about our products, product features, including AI and large language models, customers, Atlassian Marketplace, Cloud and Data Center migrations, macroeconomic environment, anticipated growth, Team Anywhere, outlook, technology, and other key strategic areas, and our financial targets such as revenue and GAAP and non- GAAP financial measures including gross margin and operating margin.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the “SEC”) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 20-F and 10- Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at https:// investors.atlassian.com.

ABOUT NON-GAAP FINANCIAL MEASURES

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit, non-GAAP operating income and non-GAAP operating margin, non-GAAP net income, non-GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled non-GAAP measures used by other companies, provide supplemental information regarding our operating performance on a non- GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

Non-GAAP gross profit. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, and restructuring charges.

Non-GAAP operating income and non-GAAP operating margin. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, and restructuring charges.

Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, restructuring charges, non-coupon impact related to exchangeable senior notes and capped calls, gain on a non-cash sale of a controlling interest of a subsidiary and the related income tax effects on these items, and a non- recurring income tax adjustment.

Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our agile & DevOps, IT service management, and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 260,000 companies of all sizes worldwide – including NASA, Kiva, Deutsche Bank, and Salesforce – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira, Confluence, Jira Service Management, Trello, Bitbucket, and Jira Align at https://atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com

Media contact: M-C Maple, press@atlassian.com

1 Gartner, Magic Quadrant for IT Service Management Platforms, Rich Doheny, Chris Matchett, Siddharth Shetty, 31 October 2022.

2 Gartner, Magic Quadrant for DevOps Platforms, Manjunath Bhat, Thomas Murphy, Joachim Herschmann, et al, 5 June 2023.

Gartner Disclaimer

Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner research organization and should not be construed as statements of fact. Gartner disclaims all warranties, express or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and MAGIC QUADRANT is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved.