Fellow shareholders,

It has been a milestone quarter for Atlassian. Eight years ago TEAM landed on the Nasdaq with just over $100 million in quarterly revenue, supporting 54,000 customers. Fast forward to today, and we’ve recorded our first-ever $1 billion revenue quarter and surpassed 300,000 customers. And while we have plenty to cheer about, there’s no time for a pit stop. We continue to take every opportunity to drive hard at our top strategic priorities: cloud migrations, enterprise, ITSM, and now, AI.

In Q2 we rolled out Atlassian Intelligence, Compass, and Virtual Agents to general availability. We were named a Leader in The Forrester Wave™: Enterprise Service Management, Q4 2023 with Jira Service Management receiving the highest possible score in the strategy category. We said g’day to Loom, welcoming them to the Atlassian family and adding async video to our toolbelt to help our customers collaborate in richer, more human ways.

As we turn up the pace of innovation across our platform, the rate at which customers are making the switch to the Atlassian cloud continues to pick up. Today, we have more seats on Cloud than on Server and Data Center combined, with migrations to Cloud in Q2 increasing more than 2x year-on-year and beating our expectations across both Enterprise and SMB.

The momentum we’re seeing into Q3 only strengthens our conviction in our long-term strategy. Our position is an enviable one: huge market opportunities, increasing commitment from customers in response to the drumbeat of innovation, a world-class team, and a unique position to combine over 20 years of insights with the immense power of AI.

There’s no time to waste. Let’s get into it!

Soaring into the cloud(s) ☁️

In a few short years, we’ve heard “whys” turn to “whens” from customers exploring a cloud migration. Since October 2020 when we announced Server end-of-support (EOS), the number of enterprise seats that migrated to cloud has increased by nearly 7x.

However, as we have always said, Server EOS is just one milestone in our multi-year migration story. Today, migrations from Data Center are driving more than 60% of cloud migrations, and we’ll only see this trend accelerate. We’re also seeing less Server churn than we had originally assumed, which means the overall migration opportunity is larger than we had expected. Server and Data Center customers are deepening their commitment to Atlassian and choosing Cloud as their final destination.

We are relentlessly executing against our cloud roadmap so customers can move to the cloud and enjoy the constant drumbeat of innovation. We’re focused on unblocking our largest enterprise customers on Data Center, ensuring the switch to Cloud is a no-brainer. In Q2 we delivered Bring-Your-Own-Key encryption for Jira Software two months ahead of schedule.

We also shipped Data Residency in Canada, on the back of delivering in Singapore and Germany. Data Residency is unlocking cloud for even more of our enterprise customers, like Mercedes-Benz who just completed a 30,000-user cloud migration:

With data centers, we had to maintain a big team who was only checking networks, seeing if servers are running, installing updates, checking availability, things like that. In the Atlassian cloud, everything is done for us, and there’s less downtime and better performance. To be competitive, we have to enable R&D, Support, and all our teams. We do that by making it easier for them to collaborate with each other and enabling them to work faster on the cloud. Atlassian cloud is the solution for high performance, high security, high availability, and the newest features.

– Mehmet Sari, Modern Collaboration Platform Team at Mercedes-Benz

And what’s more, certain departments at Mercedes-Benz enjoyed using Jira Service Management during their migration process so much, that they spotted new opportunities to apply the tool to external customer service too – an example of how easy it is to try and adopt new products in the cloud.

Picking up the pace of product progress

Q2 was a mammoth quarter across our entire product portfolio. Since introducing our Point A program in 2021, we’re chuffed to see our innovation program bear fruit (a lot of it!)

In October we launched our newest product, Compass, into general availability. As software development teams face increased complexity and responsibilities, Compass brings disconnected information and teams together in one place. With Compass, engineers can track all of their services and systems, improve software health and engineering standards through scorecards and metrics, automate consistency through software templates, and ultimately create a better developer experience. Compass was built on our cloud platform so it benefits from the analytics, automation, and AI capabilities we’ve been building, providing yet another reason for our customers to choose cloud. And with the Compass software component catalog now available directly within Jira Software, engineering teams can kickstart their developer experience initiatives and reduce context switching.

Our uptake numbers in other products born from Point A are also picking up steam, with Jira Work Management usage growing nearly 50% year-on-year, and Jira Product Discovery already surpassing 4,000 paying customers since general availability in May 2023.

We didn’t mandate the use of Jira Product Discovery, but it quickly became popular…Being able to show teams what else is going on elsewhere in the business drives a more constructive discussion and enables prioritization. It also makes it easier to ensure work aligns with business objectives.

– Charlie Duke, Senior Product Manager at Mettle

We also remain focused on enhancing the experience of every customer via the Atlassian platform with actionable insights available within Atlassian Analytics. Customers can now align people, processes, and data with end-to-end visibility of work happening across their organization via Value Stream Management Flow Metrics. In addition, engineering leaders are able to easily identify software delivery bottlenecks with DevOps Research and Assessment (DORA) dashboards to optimize a better developer experience across their entire organization.

The Atlassian tool stack has a lot of different components that you can bring together to build an end-to-end process. We’ve been able to use analytics to give us that dashboard. Now we have a platform that allows teams to communicate and make sure we have that visibility into what’s going on. We now can see defects identified, triaged, and resolved 70% faster than a year ago.

– Adam Nichols, Senior Manager, Process at DISH Networks

And since welcoming our talented Loommates at the end of November, we’ve been working on a ton of innovation in the async video space. With the rise of distributed work, we believe async video will soon be a communication mode of choice alongside text, presentations, and worksheets for the next generation of working professionals.

By combining Loom’s already passionate customer base with Atlassian’s, we have a huge cross-sell opportunity to round out the ways our customers collaborate. To supercharge this, we’ve rolled out several features in Loom set to take async video editing to the next level, with the help of AI. A call to action, an automatic share message, and simple intuitive editing to get rid of any “um’s” and “ah’s” are just some of the features we’ve added to help users get their videos looking slick and extra clickable. Sales users on our Enterprise plans can also now auto-track Loom engagement data like views, comments, and reactions all within Salesforce.

Supercharging Atlassian Intelligence

We are big believers in the power of AI to transform the way teams work. While generative AI is now readily accessible, those looking past the smoke and mirrors know it’s only as good as the data it’s fed. That’s why we believe AI will be a true differentiator and opportunity for Atlassian. We bring a huge amount of experience and knowledge about how technical and non-technical teams work; how they plan, track, deliver, and collaborate. Largely, AI tools available today are focused on individual productivity, but we believe there’s significant value we can create for our customers by building AI capabilities to supercharge teams.

We’re rolling now, with over 20,000 customers having already used Atlassian Intelligence in our Beta program. We launched the first wave of Atlassian Intelligence capabilities into general availability in the Premium and Enterprise editions of Jira Software, Jira Service Management, and Confluence, along with Virtual Agents in the Premium and Enterprise editions of Jira Service Management. Teams can now draft pages of business-critical content in seconds, automate routine tasks by asking in natural language, instantly summarize long-winded content, and more easily access relevant and context-specific help.

Atlassian Intelligence adds game-changing capabilities to our higher editions and provides another powerful reason for our customers to make the move to the cloud. We are harnessing the data we have across our products and connections to third-party tools, to deliver a differentiated AI experience that will ultimately help teams make better decisions.

We’ve always taken an optimistic yet thoughtful and long-term approach to new technologies, not becoming blinded by flashing lights, but focusing on what’s truly valuable for our customers. AI is no different. You will hear us talk more about our innovation in the AI space in the coming quarters as we build and ship unique AI experiences at a regular clip, helping teams to work better, together.

In my day-to-day work, Atlassian Intelligence acts as a virtual teammate that summarizes 5-page PIR reports into 5-sentence recaps for me, so I can get up to speed quickly ahead of monthly review meetings. It’s already proven its worth by improving productivity across our product teams.

– Matthias Hansen, Group Chief Technology Officer at Domino’s Pizza Enterprises Ltd

Celebrating our team 👏

This incredible pace of innovation can only be maintained by a truly incredible team. We were humbled to be named one of the World’s 25 Best Workplaces. This is an amazing recognition because we see it as a reflection of our people and values, helping to unleash the potential of every team.

Our Team Anywhere program is a key differentiator for employee happiness. As Atlassian ticks over 1,000 days of Team Anywhere, since then, our candidate offer acceptance rate has jumped by 20%, Atlassians are saving an estimated 10 days a year on average in commute time, and intentional togetherness gatherings are leading to a 27 percentage point increase in sense of connection – a boost lasting for four-to-five months post the event. And as distributed work isn’t just about where the work gets done, but also how, we’ve invested in tools like Loom to make async collaboration more human. To date, Atlassians have watched 3.75 million minutes of Looms, saving us an estimated 6,000+ hours of meetings.

In true Atlassian fashion, we are big on sharing our successes, challenges, and lessons learned with the world. In this spirit, we released a new report titled Lessons Learned: 1,000 Days of Distributed at Atlassian, in the hope that other teams could pull from our experiences. We want to help customers do distributed work well – and the best way to do that is to live it ourselves.

A special thanks to every single Atlassian who poured so much into 2023. Atlassian is nothing without our team. We can’t wait to reach bigger and bolder heights into 2024 and beyond

.

– Mike and Scott

Customer growth 🌱

Our customers represent diverse industries and geographies, from start-ups to blue chips, thanks to our unique flywheel model that allows us to target the “Fortune 500,000.”

We crossed another milestone in Q2, ending the quarter with over 302,000 customers, including 42,864 customers with greater than $10,000 in Cloud annualized recurring revenue (“Cloud ARR”), an increase of 18% year-over-year. The acquisition of Loom increased our total customer count by approximately 33,000 customers and increased the number of customers with greater than $10,000 in Cloud ARR by 326.

In Q2, we saw the rate at which customers convert from free instances to paid plans stabilize relative to prior quarters. This demonstrates the power of our product-led, word-of-mouth-driven flywheel that continues to add thousands of new customers each quarter. While this is a positive leading indicator for future growth opportunity, revenue contribution from new customer conversions is quite modest in our model in any given quarter.

Our mission is to unleash the potential of every team. Our cloud platform enables us to execute further on this as we continue to land new customers, as well as drive expansion within our existing base. Customers every day are realizing the incredible value that our platform delivers like Automation, Analytics, Atlassian Intelligence, and new products that are only available in the cloud. As a result, more and more customers are choosing the Premium and Enterprise editions of our cloud products to take advantage of this innovation as well as enterprise-grade functionality like greater scalability, advanced security and admin controls, and 24/7 premium support.

Security and compliance is also really critical in the financial industry. Atlassian cloud met all of our needs, which is wonderful…Plus, Atlassian is going cloud-first, and we could take advantage of all the new features, like Atlassian Intelligence. We needed to move in this direction. It was an easy sell to my executive team.

– Erica Larson, Process Engineer at Clearwater Analytics

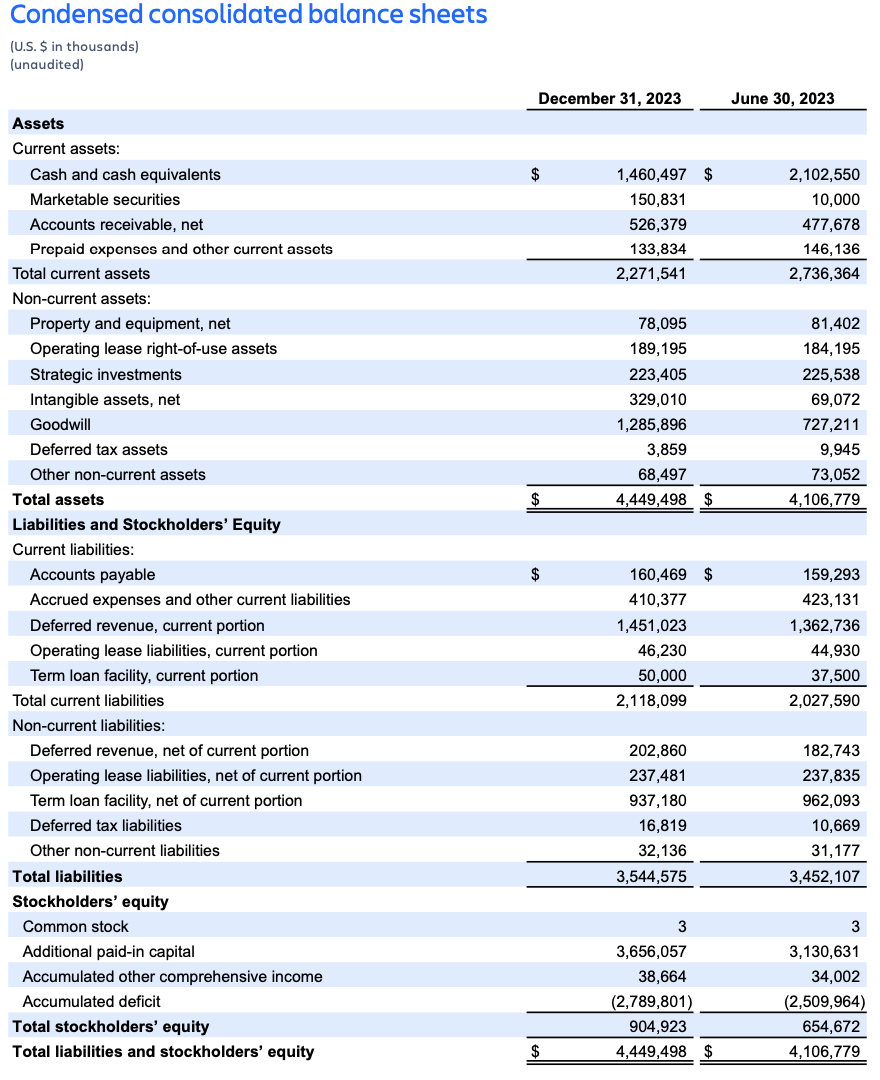

Financial highlights

Please note

Our Q2 results include the impact from the acquisition of Loom, which closed on November 30th. Loom contributed approximately $5 million of revenue and was slightly dilutive to GAAP and non-GAAP operating margin in the quarter.

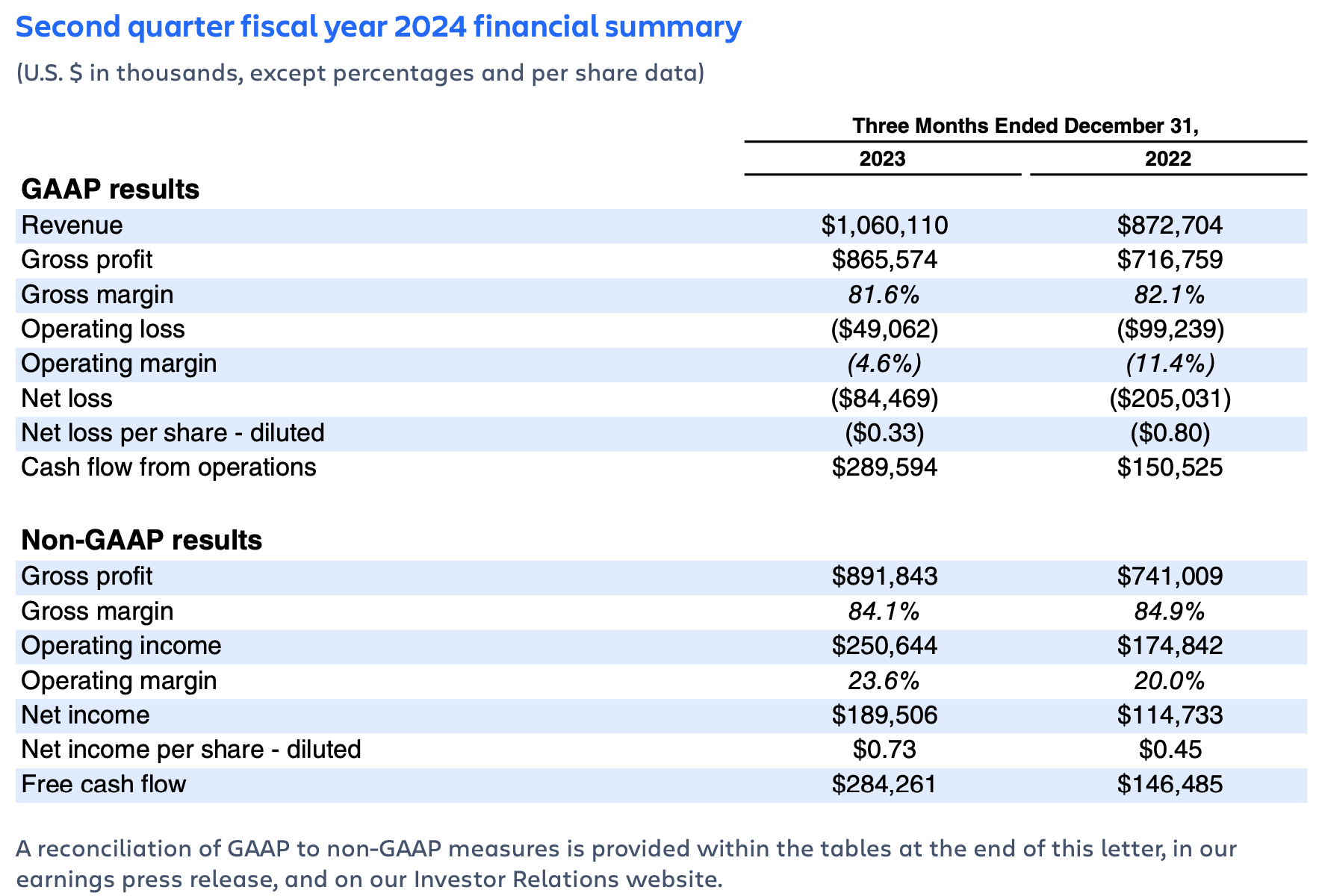

Second quarter fiscal year 2024 results

Strong enterprise sales execution and migration momentum drove revenue, gross profit, and operating income ahead of our expectations.

We achieved our first $1 billion revenue quarter as a company and delivered record billings driven by growth in our Cloud and Data Center businesses. Gross profit and operating income benefited from revenue outperformance and our continued commitment to disciplined cost management.

The momentum we are seeing across both migrations and our Enterprise business reinforces our conviction in our long-term strategy. With significant market opportunities, a great team, strong operational focus, and steady execution, we are well positioned to deliver significant value to our 300,000+ customers and drive durable, long-term growth.

Highlights for Q2’24 include:

All growth comparisons below relate to the corresponding period of last year, unless otherwise noted.

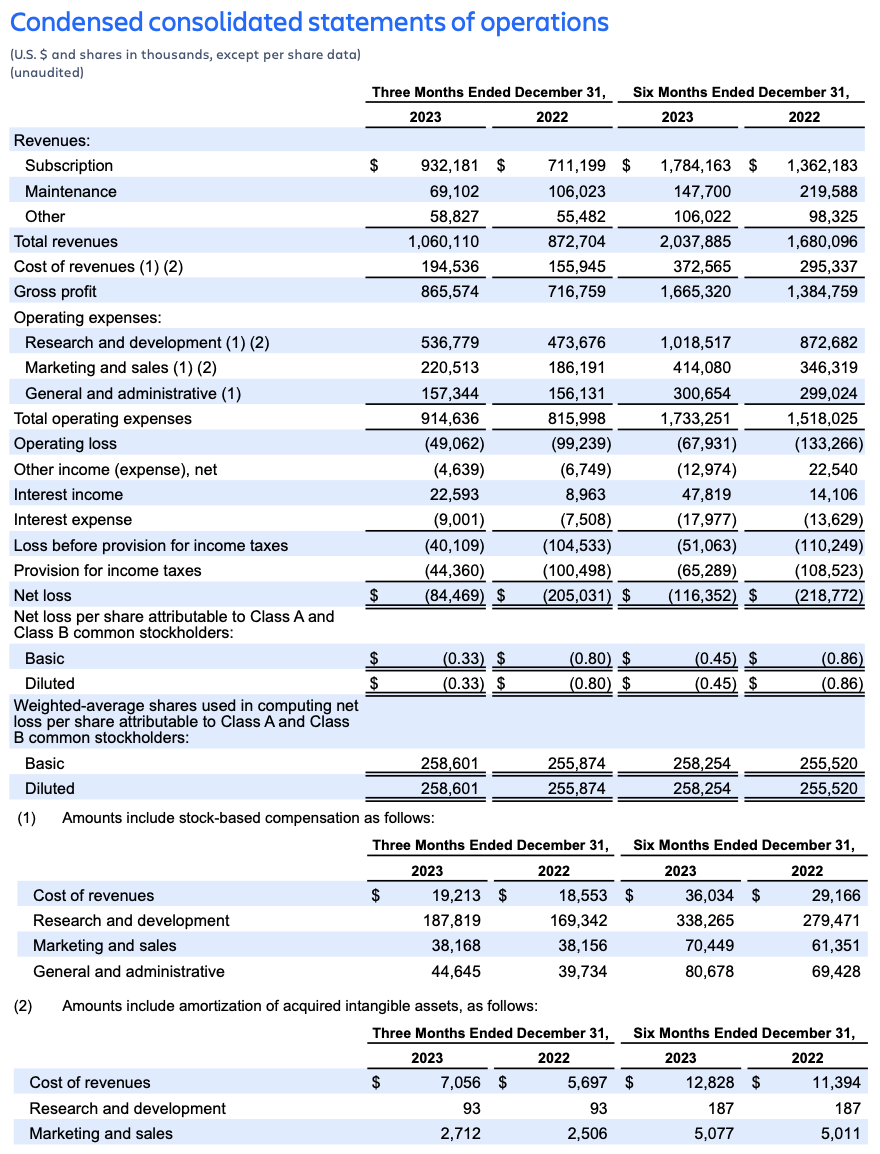

- Revenue of $1,060 million increased 21%, driven by growth in our Cloud and Data Center offerings.

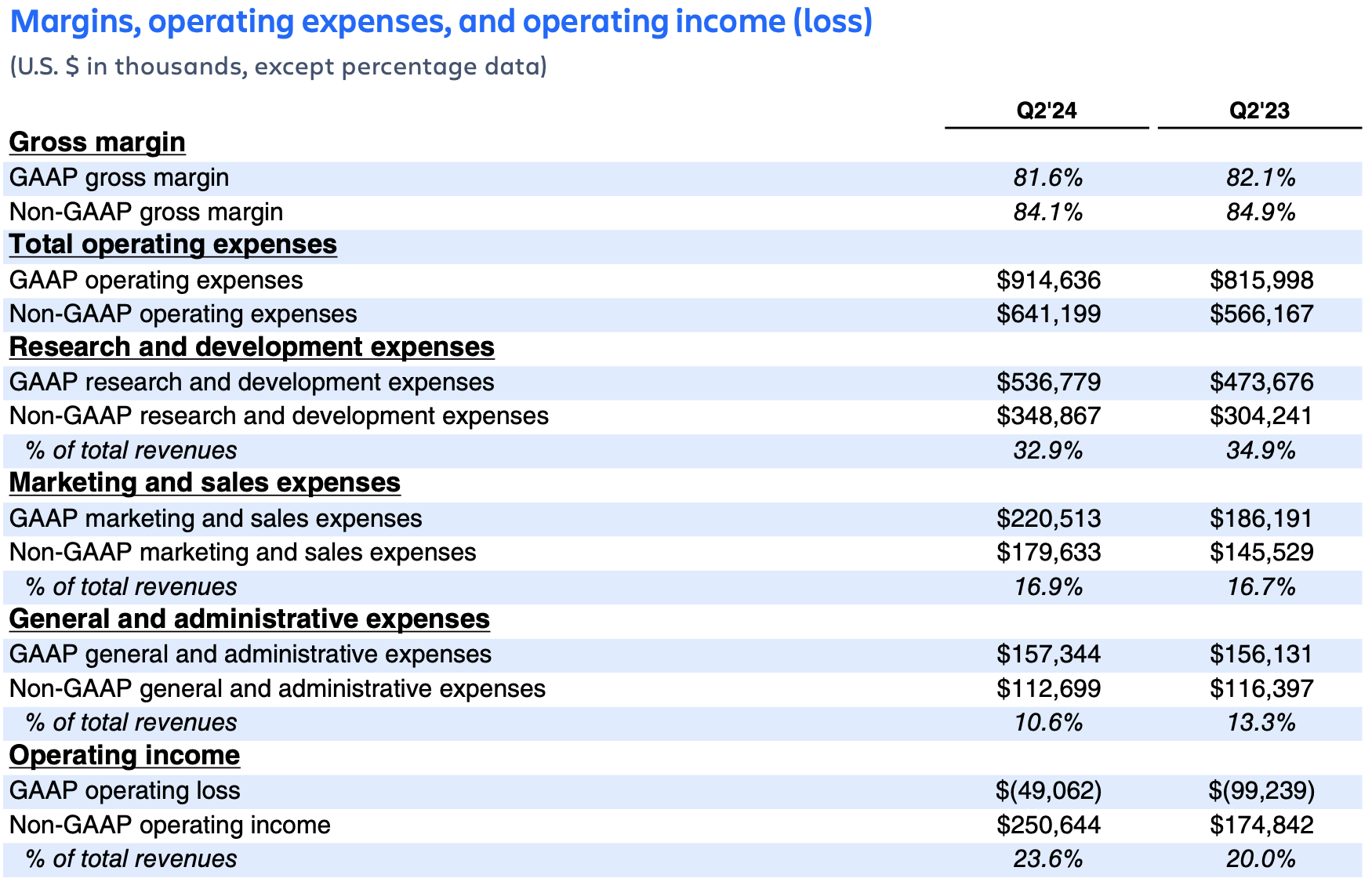

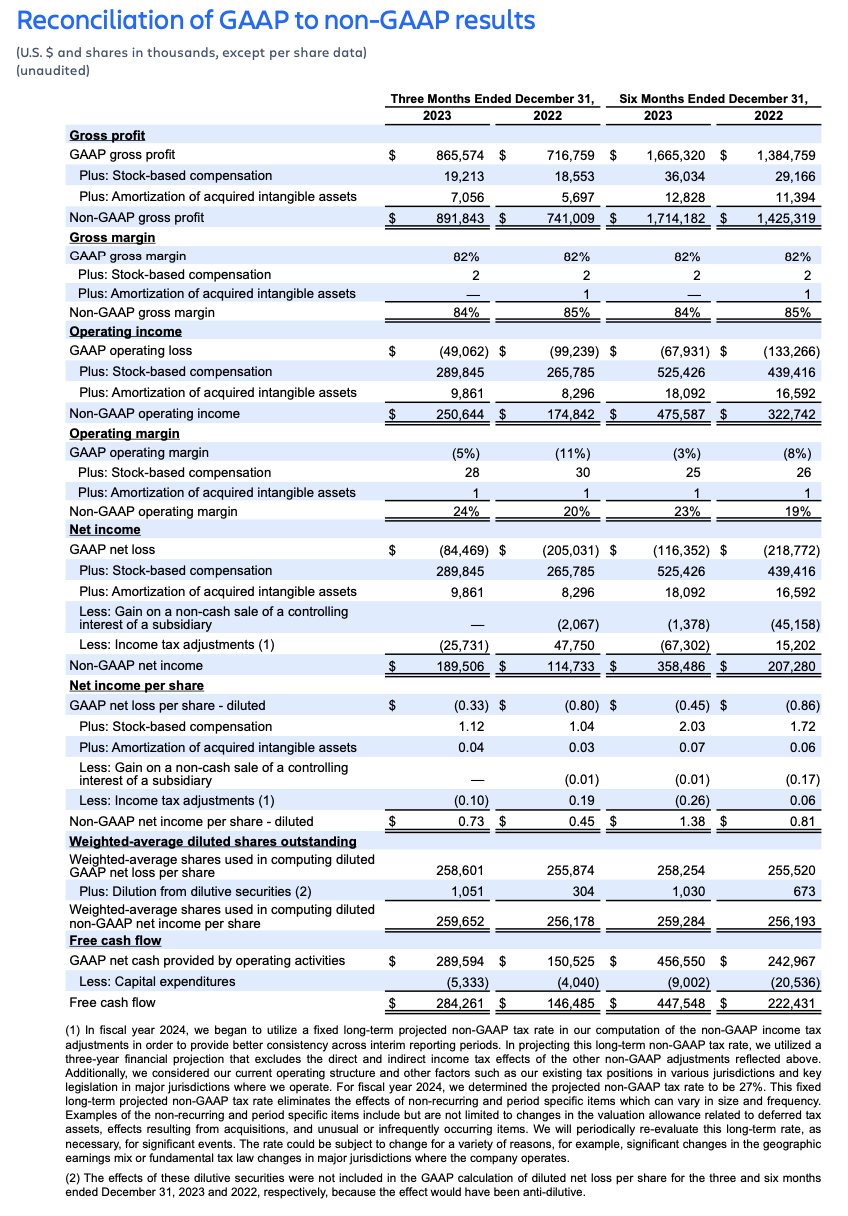

- GAAP gross margin of 82% was flat. Non-GAAP gross margin of 84% decreased approximately 1 percentage point driven by investments to support the increased demand for our Cloud offerings and the continued revenue mix shift to cloud.

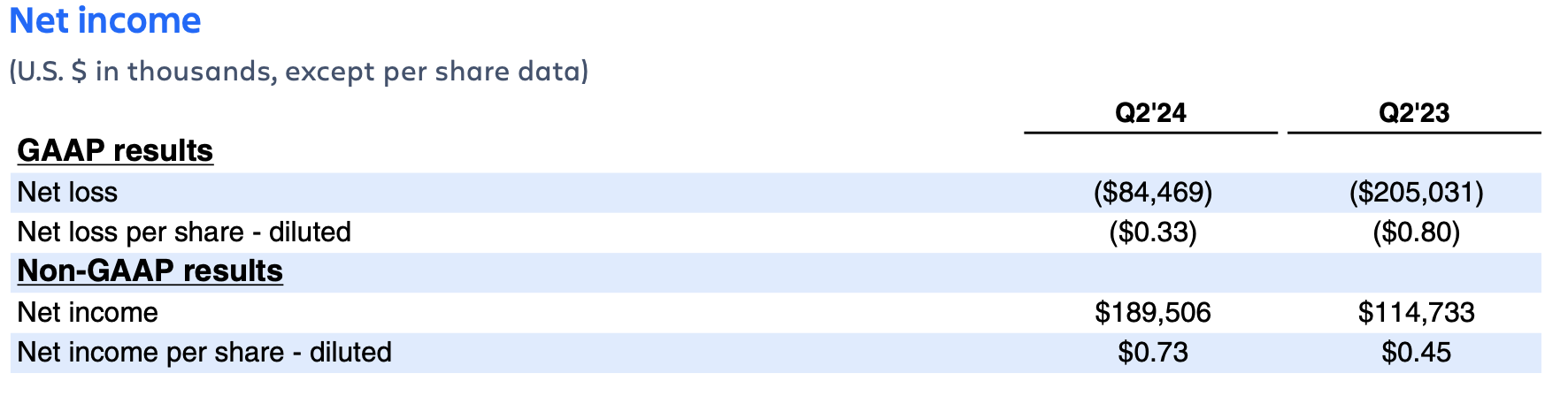

- GAAP operating loss was $49 million and GAAP operating margin of (5%) increased approximately 7 percentage points. Non-GAAP operating income was $251 million and non-GAAP operating margin of 24% increased approximately 4 percentage points driven by greater operating leverage.

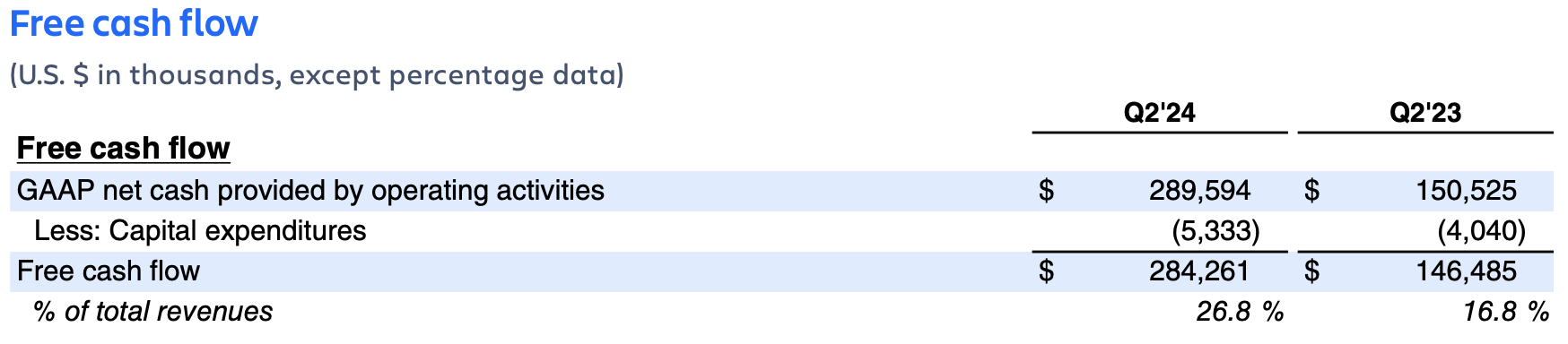

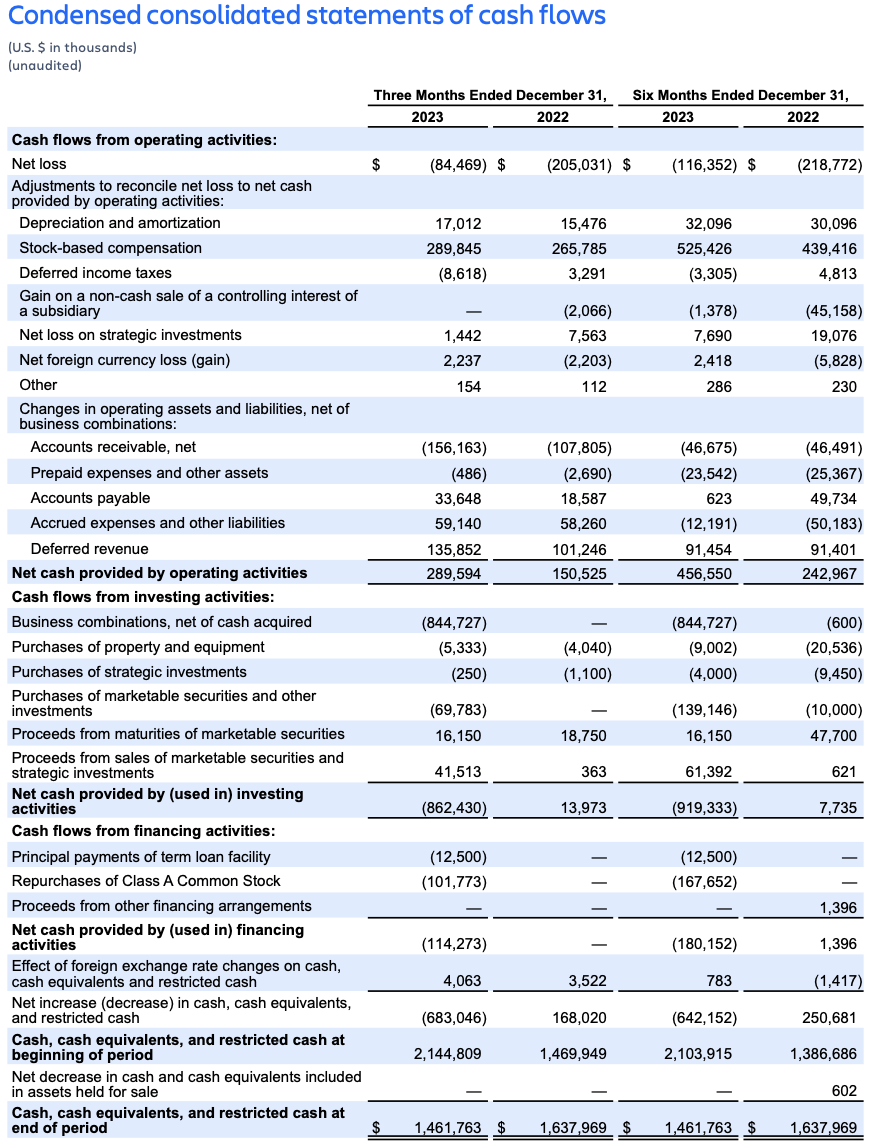

- Operating cash flow of $290 million increased 92% driven primarily by growth in collections. Free cash flow of $284 million increased 94%.

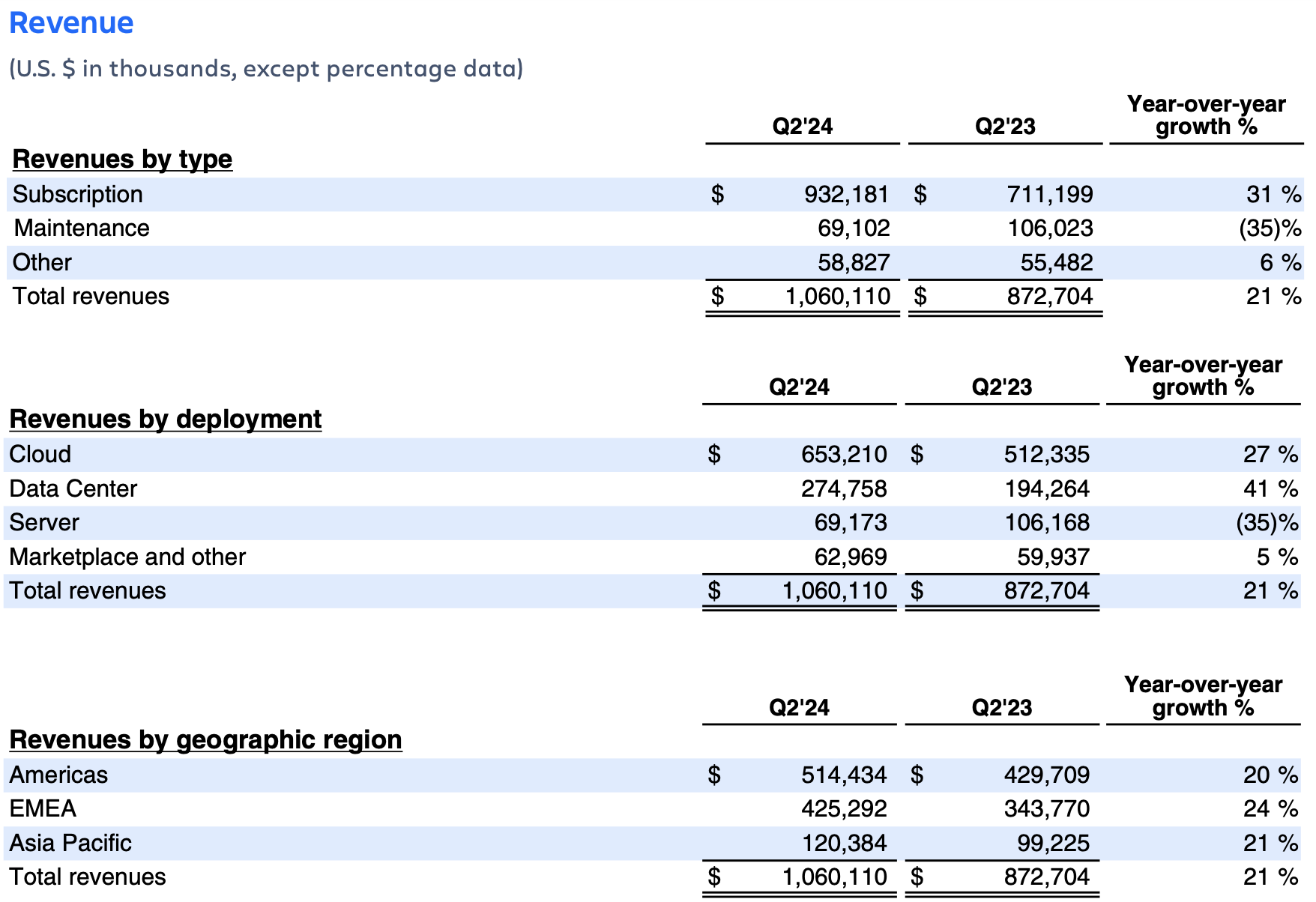

Revenue growth in Q2 was driven by subscription revenue, which grew 31%. Both Cloud and Data Center benefited from focused enterprise sales execution, which drove record billings and strong results across migrations as well as Premium and Enterprise edition sales. Our high-value, mission-critical products and services continue to drive increasing customer commitment to the Atlassian platform, yielding an increased volume of annual and large multi-year deals.

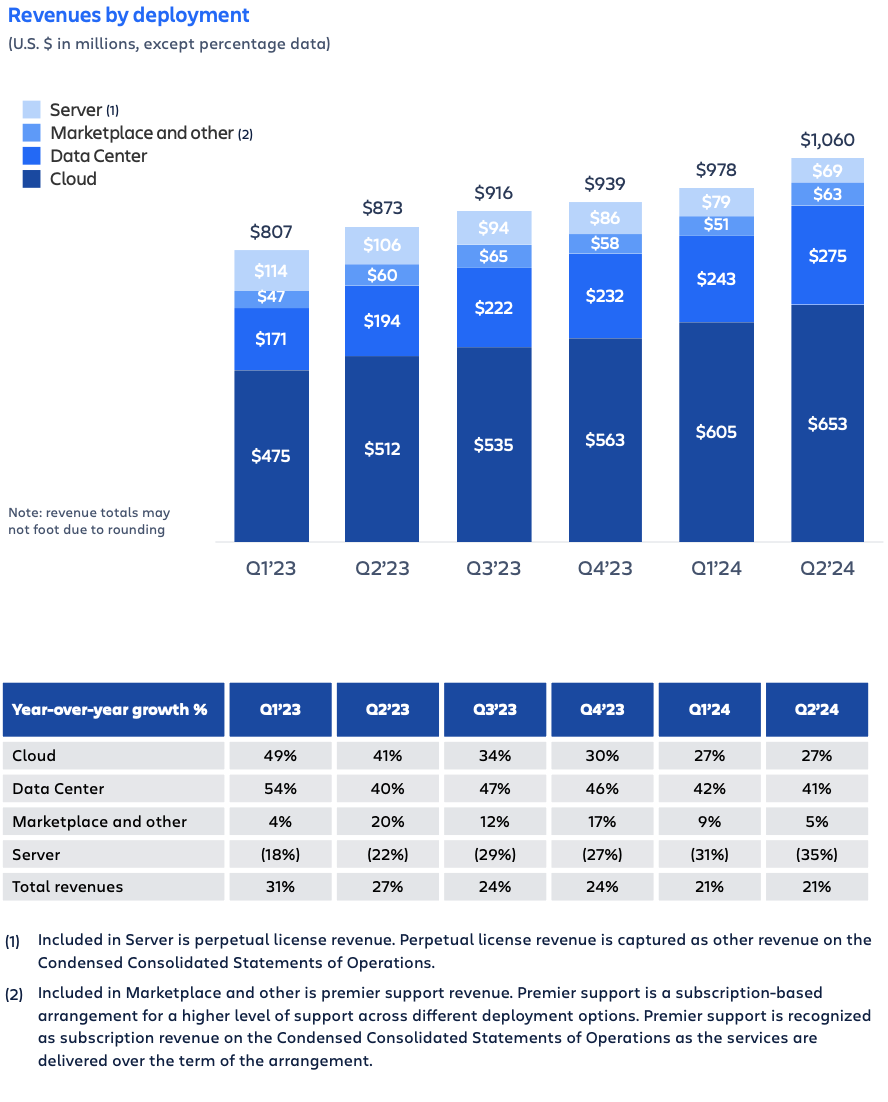

Cloud revenue growth was in line with our expectations and grew 27.5% driven by paid seat expansion in existing customers, migrations from Server and Data Center, and cross-sell of additional products. Loom contributed approximately 1 point to Cloud revenue growth in the quarter. Strong results in our enterprise customer segment driven by the enhanced enterprise-grade capabilities and innovation in our cloud platform were offset by slightly weaker-than-expected paid seat expansion in SMB and a mix shift from monthly to annual subscriptions. Importantly, migrations, cross-sell of additional products, upsell to premium-priced higher-value editions, monthly active usage, and customer retention continued to perform in line with or better than our expectations and remain healthy across our product portfolio.

Data Center revenue growth of 41% exceeded expectations driven by stronger-than-expected Server to Data Center migrations and expansion from existing customers. The impact of Server to Data Center migrations, net the impact from Data Center to Cloud migrations, benefited Data Center growth by approximately 10 points.

Lastly, deferred revenue increased 30% year-over-year to $1.7 billion driven by continued growth in the number of annual and large multi-year subscriptions.

GAAP operating expenses increased 12% year-over-year driven by higher employment costs, including bonus and stock-based compensation expenses. Headcount at the end of Q2’24 was 11,423, up 6% driven primarily by hiring in R&D and sales, as well as the addition of Loom.

Non-GAAP operating expenses increased 13% year-over-year and were slightly less than expected driven by savings in discretionary spending.

GAAP operating margin of (5%) and non-GAAP operating margin of 24% benefited year-over-year from increased operating leverage driven by healthy revenue growth, continued moderation in the pace of hiring, and focused cost management.

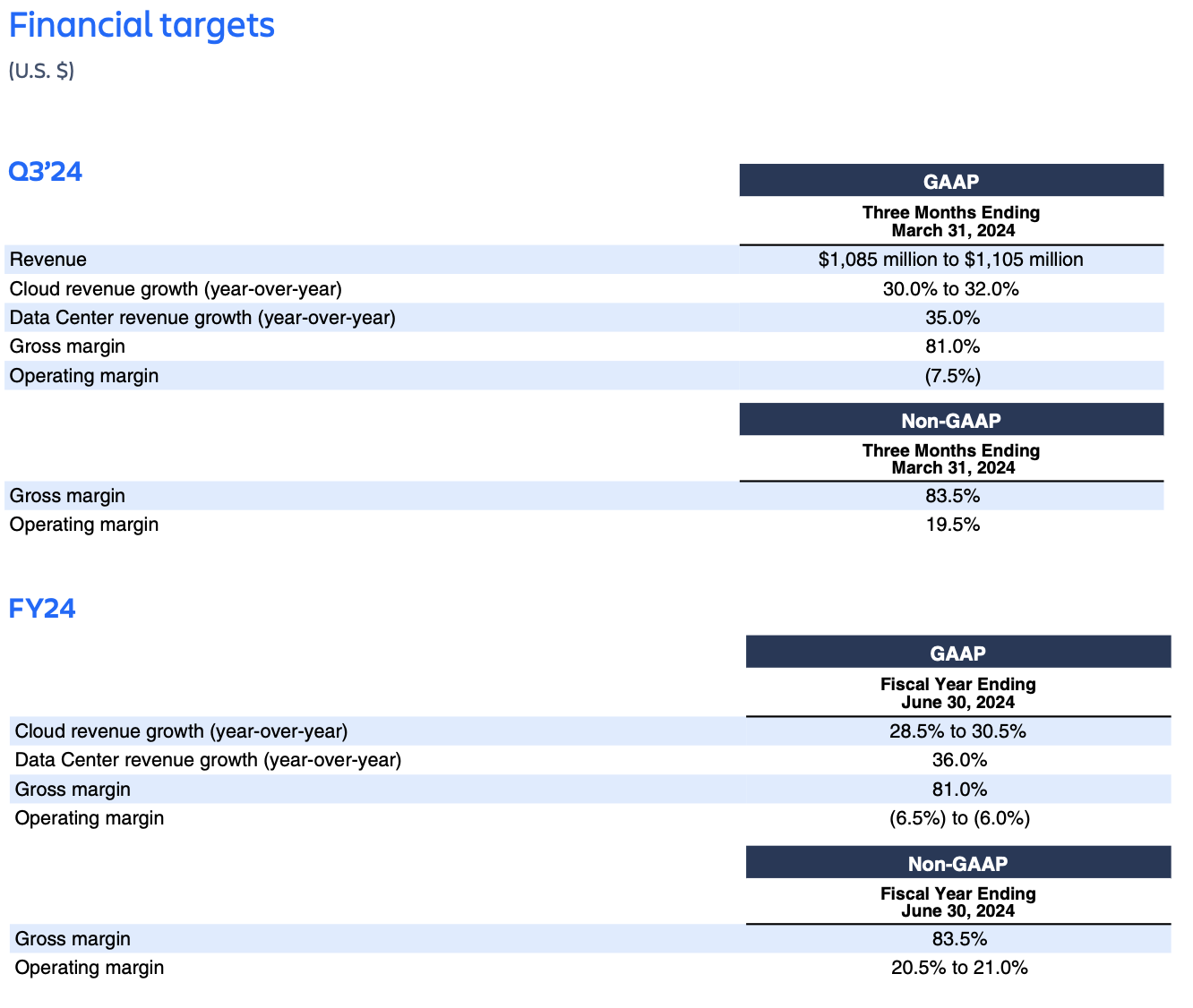

FY24 outlook

Total revenue

We have increased our FY24 revenue outlook to account for the outperformance in Q2, the strong Cloud and Data Center billings reflected in deferred revenue, and the addition of Loom.

For full year Cloud revenue, we have narrowed the range and slightly raised the mid-point of our guidance driven by migrations and performance in our enterprise customer segment. Our guidance continues to account for a range of macroeconomic scenarios in H2, with the primary impact on the rate of paid seat expansion in existing customers.

Finally, our guidance accounts for customer purchasing and migration decisions related to Server end-of-support in February, which may drive variability in our H2 results. It assumes that while some of the remaining Server customers will migrate to Cloud, the majority will migrate to Data Center, and also prudently assumes that some Server customers will not migrate in FY24. As a reminder on revenue recognition, a portion of Data Center billings is recognized up-front in the period the subscription begins while the remainder is recognized ratably over the life of the subscription. Cloud revenue, on the other hand, is recognized ratably over the life of the subscription.

Further detail and expected trends are provided below:

SUBSCRIPTION REVENUE

Cloud revenue

We expect FY24 Cloud revenue growth of approximately 28.5% to 30.5% year-over-year, of which migrations will drive approximately 10 points and Loom will contribute approximately 1.5 points of growth. Excluding Loom, the midpoint of our guidance range implies acceleration in the H2 growth rate driven by increasing Data Center to Cloud migrations and easier prior-year comparisons.

Data Center revenue

We expect FY24 Data Center revenue growth of approximately 36% year-over-year, with growth decelerating in H2 driven by declining migrations from Server, increasing migrations to Cloud, and difficult prior-year comparisons.

MAINTENANCE REVENUE

In line with our announced end-of-support for Server, we expect Server revenue to continue to decline in Q3’24. As a reminder, we will no longer recognize Server revenue beyond February 2024 and therefore expect Server revenue to be zero in Q4’24.

OTHER REVENUE

We expect Other revenue, which is primarily comprised of Marketplace revenue, to grow in the mid to high single digits in FY24, driven by continued sales mix shift to Cloud apps.

As a reminder, there is a lower Marketplace take rate on third-party Cloud apps relative to Server and Data Center apps to incentivize further cloud app development, and Marketplace revenue is recognized in full in the period of the Marketplace app sale.

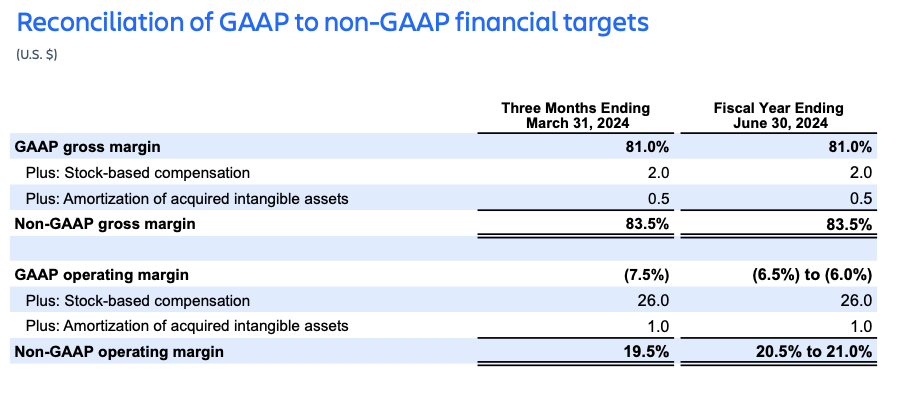

Gross margin

We continue to expect GAAP gross margin to be approximately 81.0% and non-GAAP gross margin to be approximately 83.5% in FY24. We expect gross margins to decrease in H2 of FY24 driven by continued revenue mix shift to Cloud.

Operating margin

We expect GAAP operating margin to be in the range of (6.5%) to (6.0%) and non-GAAP operating margin to be in the range of 20.5% to 21.0% in FY24. Operating expense growth will continue to be driven by our investments in key strategic priorities that drive long-term growth, such as cloud migrations, serving enterprise customers, AI, and delivering innovative customer value across our product portfolio. We have increased our FY24 GAAP and non-GAAP operating margin guidance to reflect the outperformance in Q2, changes to our H2 revenue outlook, and the acquisition of Loom, which we continue to expect to be slightly dilutive in FY24 and FY25.

SHARECOUNT

We continue to expect diluted share count to increase by less than 2% in FY24.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward-looking, including risks and uncertainties related to statements about our products, product features, including AI capabilities, customers, Atlassian Platform, Atlassian Marketplace, Cloud and Data Center migrations, macroeconomic environment, anticipated growth, outlook, technology, potential benefits and synergies from Loom and other acquisitions, our Team Anywhere program, hiring capabilities, and other key strategic areas, and our financial targets such as total revenue, Cloud and Data Denter revenue and GAAP and non-GAAP financial measures including gross margin and operating margin. We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the “SEC”) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 10-K and 10-Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

ABOUT NON-GAAP FINANCIAL MEASURES

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit and non-GAAP gross margin, non-GAAP operating income and non-GAAP operating margin, non-GAAP net income, non- GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled nonGAAP measures used by other companies, provide supplemental information regarding our operating performance on a non-GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

• Non-GAAP gross profit and Non-GAAP gross margin. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets.

• Non-GAAP operating income and non-GAAP operating margin. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets.

• Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, gain on a non-cash sale of a controlling interest of a subsidiary, and the related income tax adjustments.

• Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our agile & DevOps, IT service management, and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 300,000 companies of all sizes worldwide – including NASA, Audi, Kiva, Deutsche Bank and Dropbox – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira Software, Confluence, and Jira Service Management at atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com Media contact: M-C Maple, press@atlassian.com